Review of Recent Market Volatility & 2016 Emerging Market Outlook

The global markets’ unforeseen volatility over the past three weeks put a damper on many year-end-predictions for 2016. As we saw during the previous recent market rout in the summer of 2015, China is often scapegoated as the source of the turmoil. There are three areas in which we believe China has been misrepresented: (1) the Mainland markets’ effect on global volatility, (2) China’s currency policy, and (3) the significance of China’s “slowing” GDP growth rate. We believe an overemphasis on these three areas distract investors from other key forthcoming developments of potential great significance in 2016.

Dispelling the misrepresentations

China’s Equity Market Correlation

China’s onshore equity markets can present great potential opportunities for investors, but they can also be volatile as they were in the beginning of 2016. We were surprised by the media and market reaction to the volatility because international investors still have little exposure to these exchanges. The global markets did not rise when the onshore exchanges went up over 100% during the bull market, yet they were still somehow blamed for the recent global market weakness.

As China’s leadership pushes to open up the Shanghai and Shenzhen Stock Exchanges, the fourth and fifth largest stock exchanges globally1, China’s equity markets will no doubt play a greater role in the global economy. For now, however, we believe the perceived correlation during times of volatility produces a potential buying opportunity for Chinese companies listed outside of China. We believe U.S.-listed, Chinese securities look particularly attractive as they are largely comprised of technology companies with strong fundamentals. We previously outlined the effect of this correlation in our Tale of Two Chinas article.

China’s Currency Policy

Contrary to what many news reports might say, China is not pursuing a policy of active devaluation of its currency. Since the financial crisis of 2008, China has advocated to increase the role of the International Monetary Fund (IMF)’s reserve currency basket, known as the Special Drawing Rights (SDR). China’s leadership believes that the SDR should be more prevalently used as its own form of global reserve currency and should also be used to settle international transactions.

Beginning in December 2015, China moved to float its currency, the renminbi (RMB), in a band around the price of a basket of currencies rather than solely floating around the U.S dollar as it did in the past. Since central bank policies have kept the Euro and Yen weak compared to the U.S. dollar, the RMB depreciated inline with the value of the entire basket.

The renminbi was formally voted into the SDR basket by the IMF on November 30, 2015. The actual inclusion will commence on October 1, 2016 at which point central banks will be required to actively start trading RMB. We believe the RMB may appreciate once inclusion commences.

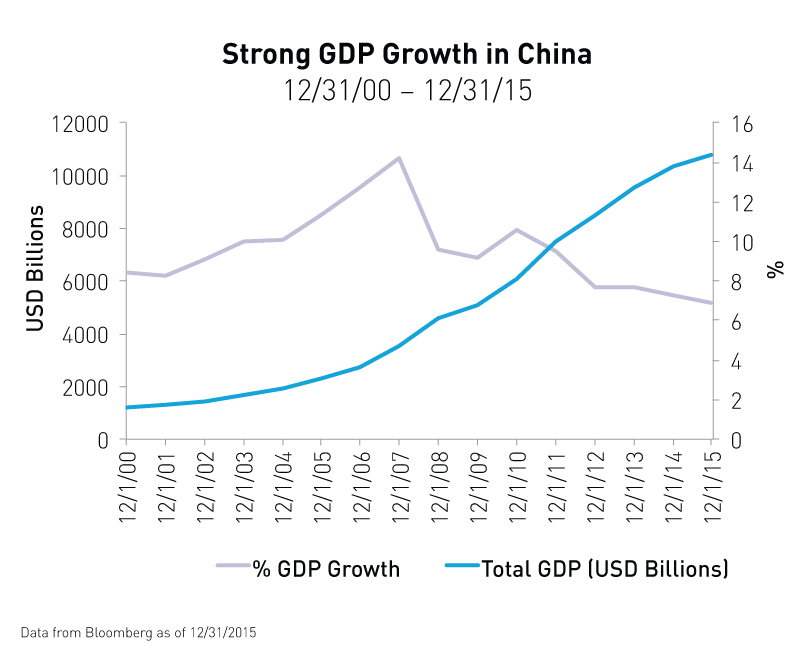

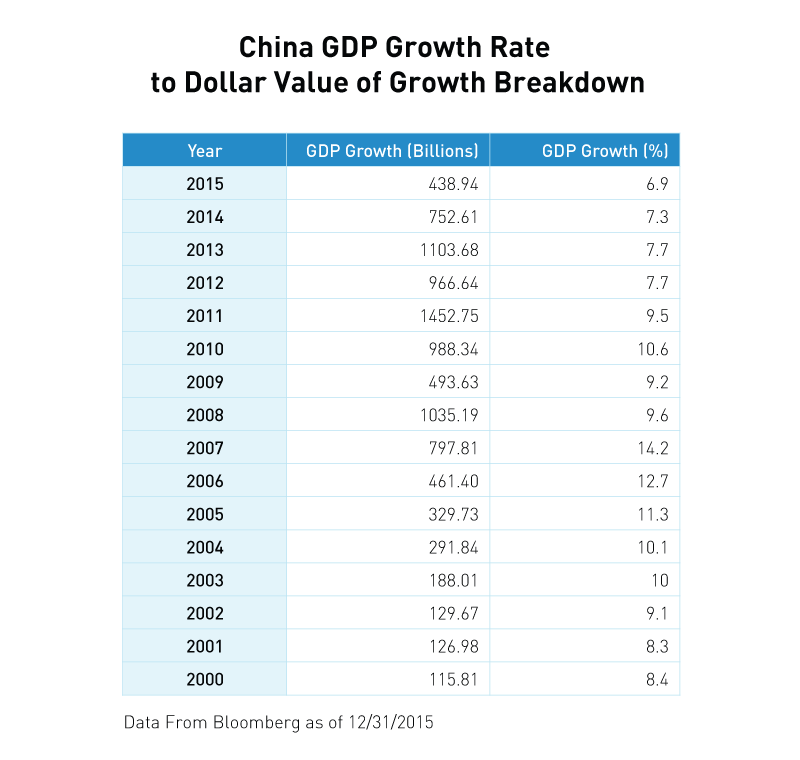

China’s “Slowing” GDP Growth Rate

On January 19th, the National Bureau of Statistics released China’s Q4 and 2015 GDP numbers, which came in at 6.8% and 6.9% respectively. The market reaction to these numbers was surprisingly negative. One headline stated, “China’s Economic Growth in 2015 Is Slowest in 25 Years”2. These negative reactions fail to account for the massive increase in the actual value the 6.9% figure represents.

In fact, the value of China’s 2015 GDP growth exceeded the value of its growth in 2005 when the rate was 11.3%. To further put things into perspective, the value of China’s 2015 GDP growth alone was greater than the entire GDP of South Africa3.

What areas of Emerging Markets should investors focus on in 2016?

MSCI will complete the second phase of inclusion of U.S.-listed Chinese companies into their indices on June 1st, which may create a surge of trading on May 31.

Emerging market investors lost billions of dollars in 2015. With that said, it may come as a shock that a China ETF, the KraneShares CSI China Internet ETF (ticker: KWEB), was on of the best performing international funds in the U.S. in 2015 according to Money Magazine4.

One factor that drove KWEB’s outperformance was its overweight to the 13 U.S.-listed Chinese companies that were included into MSCI’s global indexes as part of Phase One inclusion. On May 31, 2016 Phase Two inclusion will commence. We believe Phase Two may provide a similar catalyst to KWEB’s performance as the previous phase of inclusion. We covered the topic of index inclusion in depth in our “Power of Indexing” article.

China’s 13th Five Year Plan Will Officially Be Announced

Policy makers in China will ratify China’s 13th Five Year Plan in March. Having disseminated the draft of China’s economic blueprint last year we have a good idea of where policymakers’ focus will be.

| Theme | Description |

| Domestic Consumption | A recurring theme underscoring China’s shift from an export reliant economy to a self sufficient economy |

| Internet Plus Strategy | A government program designed to inspire technological innovation and incentivize companies in the internet and technology sector |

| Made In China 2025 | A program aimed at integrating Chinese technological advances into current manufacturing processes, especially in regard to internet of things projects. |

| One Belt One Road | A massive infrastructure project designed to strengthen trade routes abroad from both the westward land route from China through central Asia, and southerly maritime routes from China to South Asia, Africa, and Europe. |

| Renminbi Internationalization | A policy of increasing the use of the RMB in international trade and transactions. The IMF’s recent inclusion of the RMB into the SDR was a landmark achievement in support of this policy. |

| Environmental Sustainability | China will announce initiatives to cut its CO2 emissions and focus on sustainable green development and a low-carbon energy system. The government will introduce subsidies and incentives to help support clean energy companies. |

The Shenzhen Hong Kong Stock Connect will launch in 2016

The onshore markets have historically been closed off to investors outside of the Mainland. Only the largest international pension plans, foundations, and endowments were granted access via special quota systems. These systems will soon be phased out in favor of Stock Connect Programs that link the onshore exchanges with the internationally accessible Hong Kong Stock Exchange.

The first Connect Program, the Shanghai Hong Kong Stock Connect, launched in November of 2014. The second Connect Program, the Shenzhen Hong Kong Stock Connect, will launch sometime in the second quarter of 20165. Many view the pending Shenzhen Connect Program to be the final hurdle China must clear in order to get the onshore markets included within MSCI’s global indexes. We previously addressed the magnitude of this pending change in our “Power of Indexing” article. The pending inclusion presents a powerful reason to own our KraneShares Bosera MSCI China A ETF (Ticker : KBA) today.

While the global markets are off to a rocky start in 2016, we believe the pace of China’s opening up will not be slowed down. As China gets included into global indexes and institutions there will be many new opportunities created for investors in the coming year.

In order to help investors better understand how the opening of China's markets is affecting their international and emerging market portfolios, we will be publishing a series of white papers and presentations by KraneShares Managing Partner Jonathan Shelon. Mr. Shelon was the former CIO of Specialized Strategies at JP Morgan's Private Bank and former lead portfolio manager for Fidelity Freedom Funds and asset allocation portfolios. We will begin publishing Mr. Shelon's work over the course of the next several weeks. If you have an interest in this work please reach out to us.

- Data from the World Federation of Exchanges as of 12/31/2015

- MARK MAGNIER, "China’s Economic Growth in 2015 Is Slowest in 25 Years". The Wall Street Journal, Jan 19. 2016

- South Africa GDP based of 2014 World Bank Data

- "The Hottest Funds of 2015". MONEY, Dec 22, 2015

- "Shenzhen-Hong Kong Stock Connect is ready to roll out soon". China Securities Journal, Dec 11. 2015