KWEB China Internet FAQ

To help potential investors make more informed decisions, we have compiled the following responses to the top frequently asked questions we receive from our clients about the KraneShares CSI China Internet ETF (Ticker: KWEB). Additionally, we provide daily market updates through our blog China Last Night. Please click here to subscribe.

What factors influence KWEB's annual distribution levels?

Multiple factors influence the amount of distribution that KWEB makes on an annual basis. These factors can include capital gains, dividends, and unrealized gains in passive foreign investment corporations (PFICs). As KWEB has a growth investment objective, not an income investment objective, we believe that investors should reinvest distributions made by KWEB back into the strategy to align with the fund's growth-oriented investment objective.* Please consult a financial advisor or tax professional for advice relevant to your particular situation. Please see below for more details on the components of KWEB's annual distribution.

1. Dividends & Capital Gains

ETFs generally rebalance their portfolios throughout the year in order to track their underlying index. They do this by buying and selling stocks and other assets from within their holdings. ETFs are required by the US Internal Revenue Service (IRS) to pay out any net capital gains related to these transactions at least once a year to shareholders. This is called a capital gains distribution. Investors will receive their pro-rata distribution in proportion to the number of shares they hold. ETFs are also required to distribute any cash dividends paid by the underlying holdings.

2. Passive Foreign Investment Corporations (PFICs)

ETFs that invest in international stocks may own shares in companies that are treated as Passive Foreign Investment Companies (PFICs). PFICs are defined as non-US corporations with at least 50% of their assets invested in cash or passive investments, or with 75% or more of their gross income derived from passive sources, including interest, dividends, and rents. Performance of companies classified as PFIC is marked-to-market, and unrealized gains are counted toward ordinary income distribution requirements.

Please note that all foreign companies are subject to PFIC tests, and the companies' own auditors determine if they are classified as a PFIC.

Ten companies contributed to PFIC-related distributions for KWEB this year, and these companies accounted for over 25% of KWEB's total assets.10 According to preliminary estimates, PFIC-related could represent a significant portion of the year-end KWEB distribution in 2025.

Does KWEB have exposure to artificial intelligence (AI)?

Yes. We believe KWEB holdings represent a good way for investors to gain access to AI opportunities in China. Unlike in the United States, where private companies such as OpenAI are leaders in AI innovation, China's AI development is primarily led by publicly traded internet platforms. Some examples include Alibaba, whose Qwen large language model (LLM) is a popular in China, Baidu's ERNIE bot, which is linked to the company's existing traditional search product, Kuaishou's Kling AI, a global video generator, and Tencent's Hunyuan LLM. Most of these platforms offer their models for free and then seek to generate revenue from demand for cloud services. We estimate that AI-related services contributed 6% to the overall revenue earned by KWEB's holdings in 2024.

What are some potential near-term catalysts for KWEB?

- The 15th Five-Year Plan, to be released officially in the first quarter of 2026, places emphasis on technology self-sufficiency, especially regarding artificial intelligence,7 which make it likely that KWEB companies could receive significant support in the coming years.

- China’s government continues to seek to reduce urban unemployment3 and increase domestic demand in the form of consumer spending, and China’s internet giants should play an integral role in achieving these goals.

- KWEB’s long-term growth story remains intact. China’s internet population continues to grow, adding 16 million new users in 2024, and China’s internet companies continue to grow their revenues, as the fund's top ten holdings (as of 6/30/2025) increased revenue by an average of 11% year-over-year in the second quarter of 2025.9

- We believe the continued beneficial impact of China's consumer recovery on the revenues of China's E-Commerce and internet-related industries, the transmission engines of China's consumer economy, could benefit KWEB.

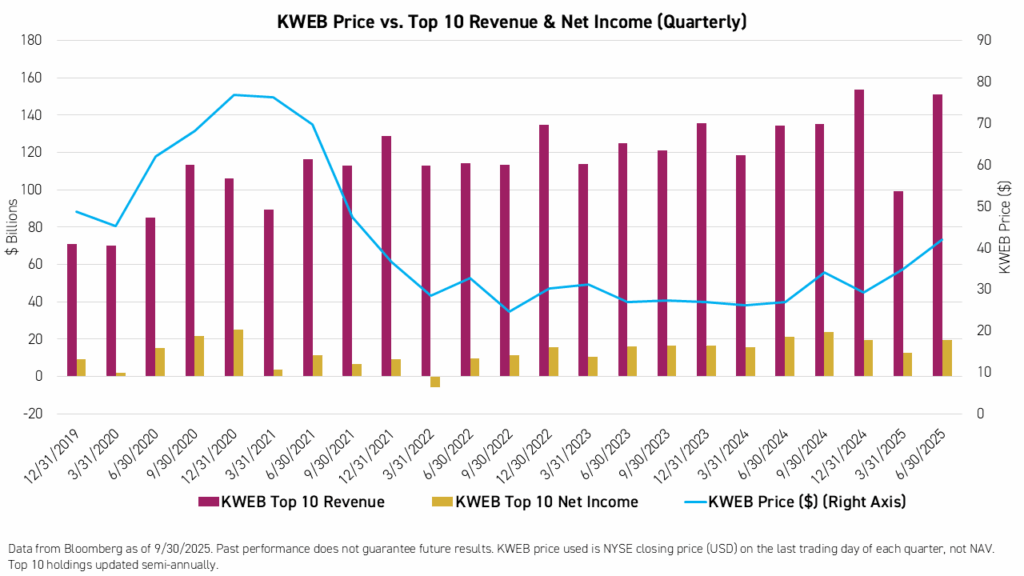

As the chart below demonstrates, many of KWEB's top ten holdings continue to be significantly below their all-time high prices.

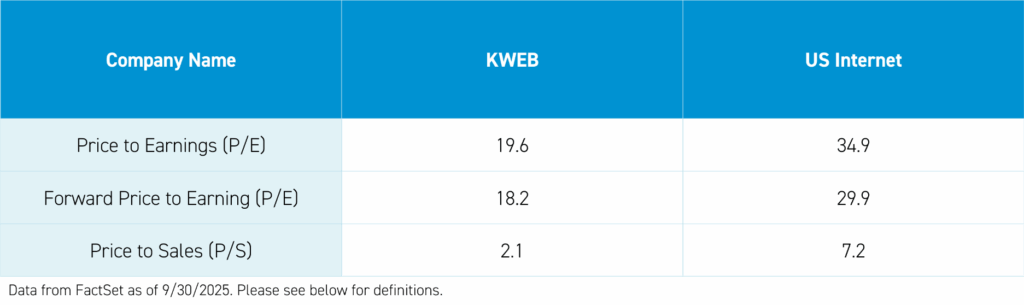

What about KWEB's fundamentals?

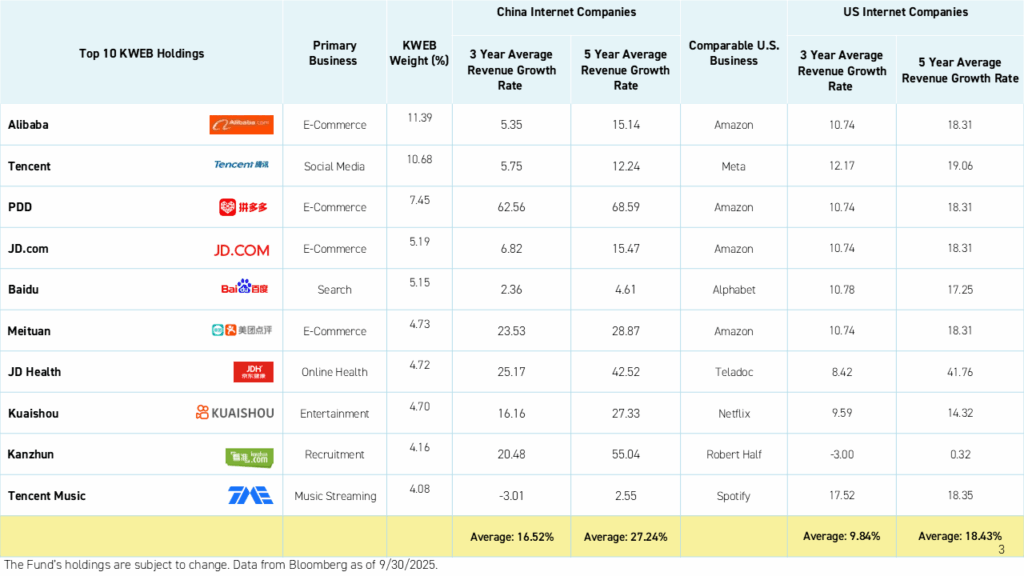

- The 3 & 5-year average revenue growth rates for China internet companies are similar to those of many U.S. internet companies.

- However, companies in KWEB continue to trade at, on average, 50% lower multiples versus their US peers.

- We believe that most of the price action in KWEB in recent years has not been fundamentally driven.

How do US-China relations affect KWEB?

Headline news surrounding the US-China relationship can negatively impact investor sentiment around KWEB and its underlying holdings, injecting volatility into the China internet space. However, the revenues of KWEB companies are mostly derived from China's consumer economy and do not depend on trade with the US.

Nonetheless, the Trump Administration continues to make progress on a trade agreement with China. The White House announced that, effective November 10th, the tariff rate on China will be cut from 34% to 10% and the fentanyl-responsive tariff will be cut from 20% to 10%.5 This was followed by an announcement from China's Ministry of Finance that, effective November 10th, the 24% additional tariff rate on US goods will remain suspended for one year.6 Also, President Trump has scheduled a state visit to China in April of 2026.

What are some options for investors that are concerned about KWEB's volatility?

We believe the following are feasible options for investors who believe in the China internet industry's long-term prospects but are concerned about short-term volatility in KWEB and its underlying holdings.

- Dollar Cost Average**: Rather than allocating to KWEB all at once, investors can spread their investments over time, buying at designated intervals or following KWEB price declines. For investors unfamiliar with this practice, Schwab has an excellent personal finance article that covers the topic in-depth.

- Put volatility to work with a covered call strategy: Investors can purchase shares in the KraneShares China Internet & Covered Call ETF (Ticker: KLIP) alongside their KWEB investment. With covered call ETFs, increases in volatility typically see corresponding increases in the yields these strategies provide. KLIP exchanges the uncertain upside of KWEB for premium income that helps to shield the downside. Please click here to learn more.

- Use our new defined outcome strategies: The KraneShares 100% KWEB Defined Outcome January 2027 ETF (Ticker: KPRO) aims to match the performance of KWEB to a predetermined cap of 20.01%, with a 100% downside buffer. Meanwhile, the KraneShares 90% KWEB Defined Outcome January 2027 ETF (Ticker: KBUF) aims to match the performance of KWEB to a predetermined cap of 40.01%, with a 90% downside buffer.

KPRO and KBUF have characteristics unlike many traditional investment products and may not be suitable for all investors. For more information regarding whether an investment in the Funds is right for you, please read the Funds' prospectuses including "Investor Suitability Considerations".

What is the Holding Foreign Companies Accountable Act?

Congress passed the Holding Foreign Companies Accountable Act (HFCAA) in December of 2020. The law requires all US-listed foreign companies to allow the Public Company Accounting Oversight Board (PCAOB) to inspect their audit books, disclose government ownership, if any, or face delisting. The law only applies to listed stocks, not ETFs, so KWEB is not at risk of being delisted under this law.

On December 15th, 2022, auditors from the Public Company Accounting Oversight Board (PCAOB) gained complete access to inspect and investigate auditors in Hong Kong and Mainland China, bringing these auditors and the companies that they audit, which include KWEB holdings, into compliance with the law.1 We believe this historic development significantly reduced the delisting risk for US-listed Chinese stocks.

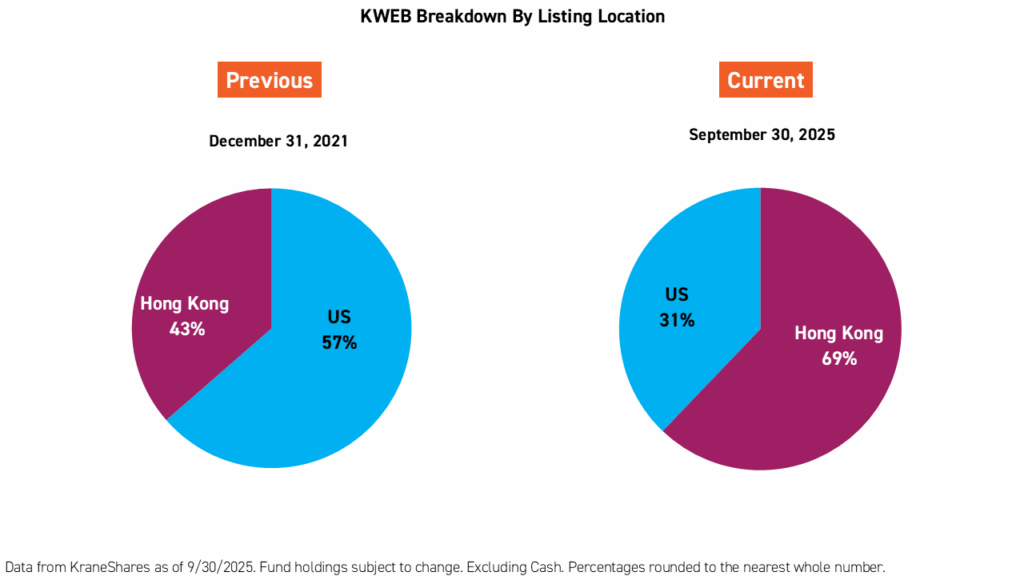

Is KWEB still converting US listings of holdings to Hong Kong listings?

Following the improvement in audit access in China, which is described above, KraneShares will maintain its current level of exposure to US listings. This decision also follows our conversations with executives from multiple KWEB holdings, who are confident in the status of their US listings. Furthermore, many companies that were originally planning on either cross-listing in Hong Kong for the first time or converting their existing secondary listing in Hong Kong to a dual-primary listing, as was the case with Alibaba, have put their plans on hold. As such, KraneShares has paused the conversion of American depositary receipts (ADRs) into Hong Kong-listed shares, a process that began in 2021. We may resume conversions at a later date if these conditions change.

Nonetheless, a majority of the Fund (69%) is currently (as of 9/30/2025) allocated to Hong Kong listings.

What are the potential benefits to companies listing in Hong Kong?

There are many potential advantages for a US-listed company to have a secondary of dual primary listing in Hong Kong. US and Hong Kong share classes are fungible, meaning shares can be freely converted from one listing location to another, as long as your broker allows for such a conversion. KraneShares' professional management team handles the conversion of US-listed stocks into Hong Kong shares for KWEB's holdings on behalf of our clients.

One key benefit of having a dual primary or primary listing in Hong Kong is that having such a listing enables Mainland Chinese investors to access these stocks, often for the first time, via Southbound Stock Connect. This could mean significant inflows to companies like Alibaba, who announced their Hong Kong dual primary listing in late July 2022. For reference, Tencent is listed in Hong Kong and accessible to Mainland investors via Southbound Stock Connect. As of December 1, 2025, Mainland investors held 11.1% of Tencent's shares outstanding.4

*Reinvesting distributions increases exposure to market fluctuations and may lead to losses. There is no guarantee reinvestment will improve returns. Consider your goals and risk tolerance before choosing this option.

**Dollar cost averaging does not guarantee against a loss and is not a solution to investment risk. As markets tend to rise over time, you may do better if you invest a lump sum earlier.

Citations:

- Williams, Erica Y. “PCAOB Secures Complete Access to Inspect, Investigate, Chinese Firms for First Time in History,” Public Company Accounting Oversight Board (PCAOB) News Release. December 15, 2022.

- Franck, Thomas. “Treasury Secretary Yellen sees no need for China sanctions as US tries to deter aid to Russia,” CNBC. March 25, 2022.

- Release From the People's Republic of China, National Party Congress (NPC) dated March, 2024.

- Data from Hong Kong Exchanges & Clearing as of 12/1/2025.

- The White House as of 11/10/2025.

- Ministry of Finance as of 11/10/2025.

- "China's new five-year plan sharpens industry, tech focus as US tensions mount," Reuters. October 23, 2025.

- Data from the National Bureau of Statistics of China as of 12/31/2024

- Data from KraneShares and Bloomberg as of 6/30/2025

- Data from KraneShares as of 12/10/2025.

Definitions:

Dow Jones US internet Composite Index ("US Internet"): The Dow Jones Internet Composite Index is designed to measure the performance of the 40 largest and most actively traded stocks of U.S. companies in the internet industry. To be eligible for the index, a company must derive at least 50% of cash flows from the internet. The index was launched on February 18, 1999.

CSI Overseas China Internet Index: CSI Overseas China Internet Index selects overseas listed Chinese Internet companies as the index constituents; the index is weighted by free float market cap. The index can measure the overall performance of overseas listed Chinese Internet companies. The Index is within the scope of the IOSCO Assurance Report as at 30 September 2018. The index was launched on September 20, 2011.

Price to Earnings: The price-to-earnings ratio (P/E ratio) is the ratio for valuing a company that measures its current share price relative to its per-share earnings (EPS). The price-to-earnings ratio is also sometimes known as the price multiple or the earnings multiple.

Forward Price to Earnings: Forward price-to-earnings (forward P/E) is a version of the ratio of price-to-earnings (P/E) that uses forecasted earnings for the P/E calculation. While the earnings used in this formula are just an estimate and not as reliable as current or historical earnings data, there is still benefit in estimated P/E analysis. The Forward P/E ratio for the fund is not a forecast of the fund's future performance.

Price to Sales: The price-to-sales ratio is a valuation ratio that compares a company’s stock price to its revenues. It is an indicator of the value that financial markets have placed on each dollar of a company’s sales or revenues.

Dividend Yield: The sum of a company's dividends paid out over the prior year per share divided by the company's share price.

Revenue Growth: Revenue growth is the percentage increase in a company’s total revenue over a specific period, such as a quarter or a year. It measures how much a company’s sales or income has expanded compared to a previous period.

2026 Emerging Technology Outlook: Bull Market Broadening?

KraneShares’ KWEB ETF Lists in Hong KongKraneShares Connects NYSE to ADX with the First US ETFs to Cross List in the RegionBABA’s Cloud, XPEV Going ‘Full Tesla’ & State of China’s Tech TradeSchwab Network: Henry Greene on China Internet Companies’ Q3 Results & KWEB