Can AI Chip Design Help Baidu & Alibaba Unlock Shareholder Value?

By  Henry Greene

Henry Greene

In the age of AI, hardware is crucial. Large language models (LLMs) and other AI systems demand extreme amounts of computing power. Seemingly, the only limitation to their development is the quantity and quality of the chips that they can access.

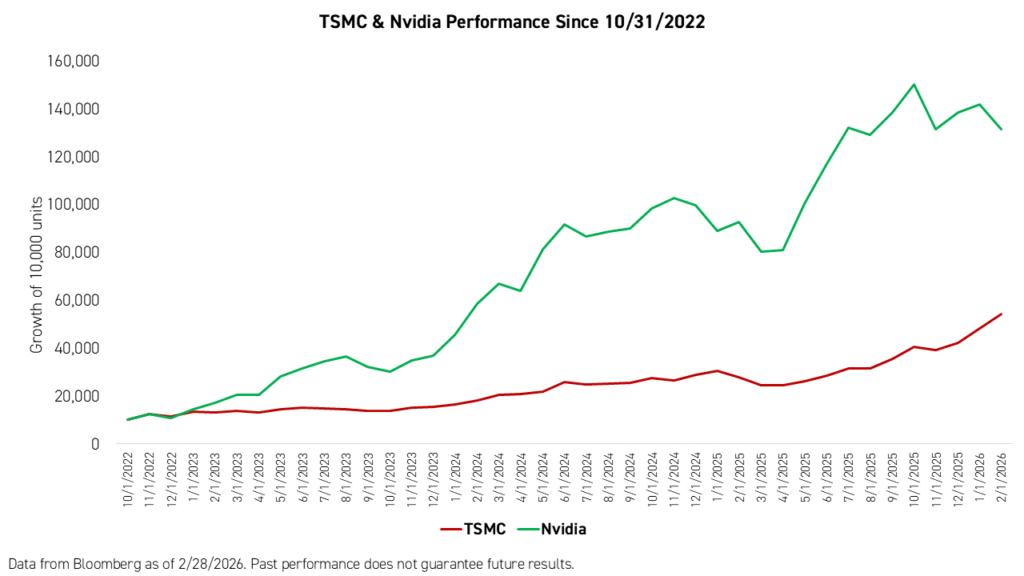

The valuations of the world’s largest chip designers and manufacturers are a testament to the importance of chips to AI development. Taiwan Semiconductor Manufacturing (TSMC) is a key manufacturer, or fabricator, of the high-end microchips that AI systems run on, and has seen its share price increase 429% since Chat GPT launched in November. Meanwhile, Nvidia, a key chip designer, also known as a fabless chipmaker, has seen its share price rise 1,270% since ChatGPT was launched.

Facing an uncertain supply of high-end chips due to US export restrictions under the Biden administration, Alibaba and Baidu invested heavily in their own chip design capabilities. Today, these ventures have the potential to help them unlock significant shareholder value. A simple Sum of The Parts (SOTP) analysis of Baidu and Alibaba, including their respective chip design arms, Kunlunxin and T-Head, suggests markets may not be valuing these internet giants properly. Although chip design accounts for a small portion of revenue for both companies, if these businesses could command the same valuation multiples as global peers like Nvidia or China-based fabless peers like Cambricon, both businesses would be worth significantly more.

Sum of The Parts (SOTP) Analysis of Baidu & Alibaba

Baidu and Alibaba represent full-stack AI ecosystems, generating value across models, cloud, and now semiconductors. These capabilities were added on top of existing businesses in advertising and E-Commerce for Baidu and Alibaba, respectively, making these companies conglomerates. Baidu’s new technological edge is also added on top of a relatively mature robotaxi business: Apollo Go.

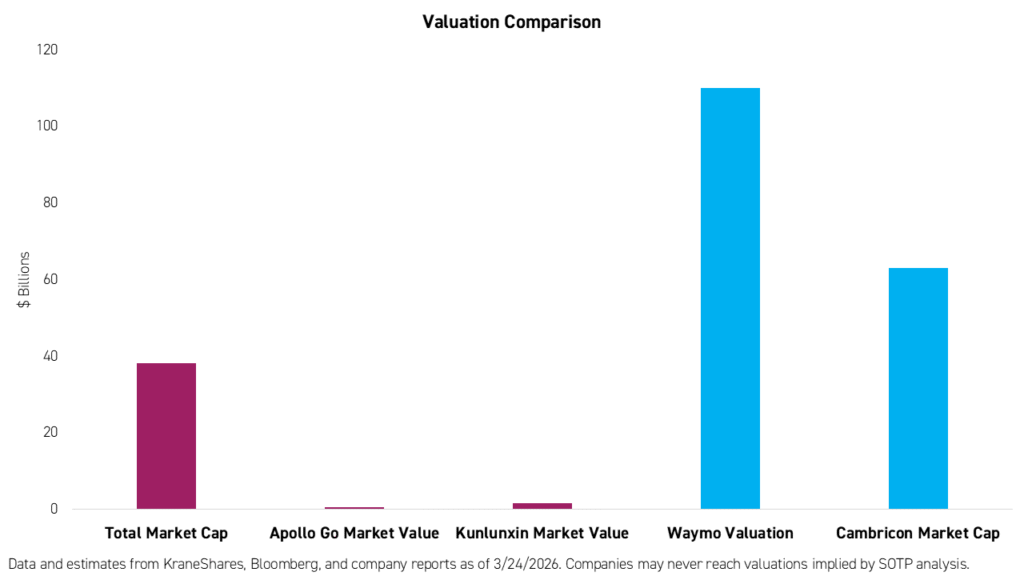

Starting with Baidu, we conducted a sum of the parts analysis to find the implied market valuation of its businesses, derived from Baidu's overall market capitalization and assumptions about these businesses' contribution to overall revenue. Baidu's chip design unit Kunlunxin and its robotaxi unit Apollo Go appear undervalued compared to the valuations the markets are currently applying to comparable businesses Cambricon and Waymo, for chip design and robotaxis,2 respectively.

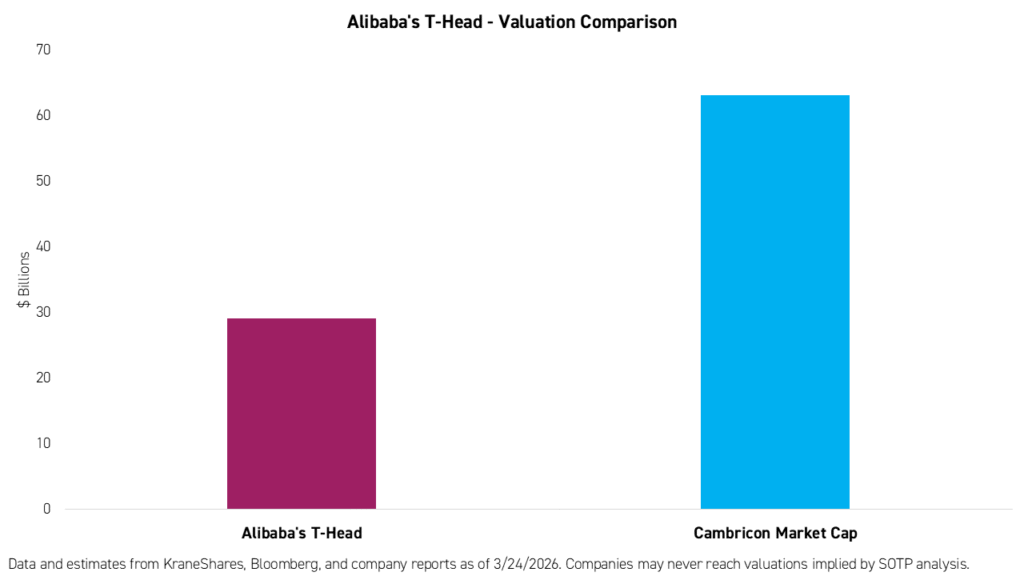

Alibaba appears to be in a similar situation with at least one of its business units. Its chip design unit T-Head, if valued at a fraction of Alibaba's market cap proportionate to its revenue contribution, is also worth considerably less than Cambricon.

Exploring The Differences Between T-Head & Kunlunxin

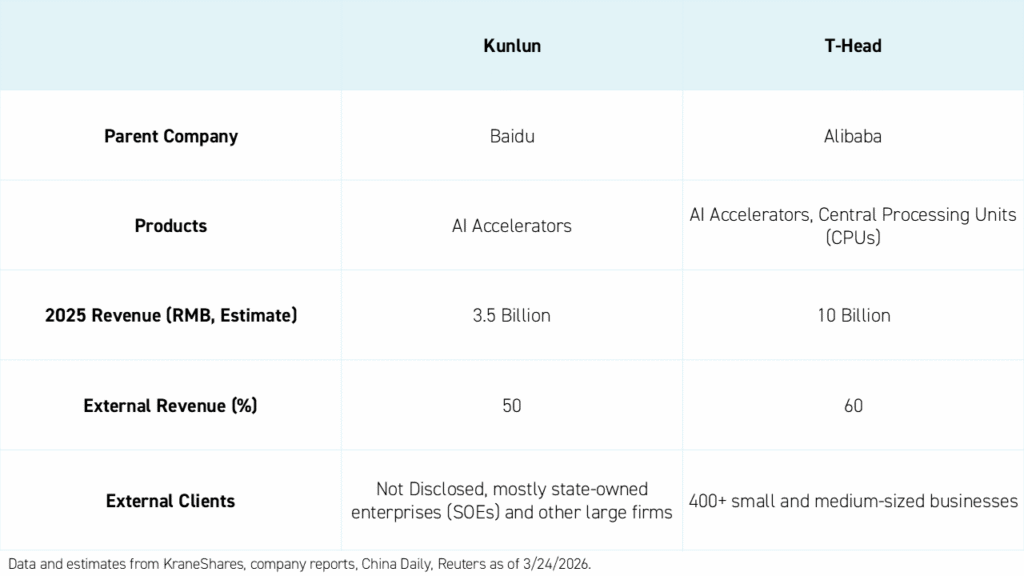

T-Head and Kunlunxin are both fabless semiconductor companies, meaning they do not manufacture their own chips. Rather, they are customers of fabricators such as TSMC, focusing instead on chip design. Kunlunxin is estimated to have generated $500 million in revenue in 2025.3 Its revenue mix is currently split evenly between externa customers and chips for internal use within Baidu’s massive cloud server network. China Mobile, one of China’s largest mobile phone carriers, is a key customer. The mobile provider wwas also a key strategic investor in the unit, valuing it at $3 billion when it invested in a funding round in mid-2025.3 Kunlunxin's product focus is purely on AI accelerators, specialized chips meant to speed up inference operations.

T-Head is estimated to have generated $1.5 billion in revenue in 2025. Like Kinlun, T-Head benefits from both external and intrernal demand. However, T-Head receives approximately 60% of its revenue from external customers, whereas Kunlunxin only received 50% of its revenue from its external customers.

Although both Kunlunxin and T-Head have developed niches and established strong domestic, internal, and external consumption pipeline for their products, the status of US export controls may affect their performance. China approved a first batch of H200 Nvidia chips for ByteDance, Alibaba, and Tencent in mid-January this year, after the Trump Administration departed from the previous US Administration’s stance of completely restricting the export of higher-end AI chips. However, the extent to which Nvidia chips will be available in China remains uncertain, and Kunlunxin and T-Head could step in to make up for lost demand, when necessary. The continued uncertainty of overseas chip availability to China-based customers remains an opportunity for these players, alongside Cambricon.

Potential Spin Off Scenarios

Baidu has already filed for a Hong Kong IPO of Kunlunxin. However, Alibaba has not indicated any intended change for T-Head within its corporate structure.

Below are three possible spin-off scenarios for Kunlunxin and T-Head.

Scenario #1: The parent companies could choose to keep the IPO float low and maintain a large stake, potentially a controlling one, in the business. If the spinoffs are in high demand with investors, this is an ideal strategy, as the companies would benefit most from the potential appreciation of the floated shares. This would be similar to how JD.com maintained a 50% ownership stake in its own logistics business after spinning it off as JD Logistics through a Hong Kong IPO in 2021.4

Scenario #2: The parent companies could float the entirety of their fabless chipmaking units on the Hong Kong Stock Exchange and not keep a meaningful stake. We believe this is unlikely, as the units are relatively small and will find it difficult to attract sufficient outside investor demand to lead to the valuations mentioned above on their own. This would lead to a potential one-time windfall for the companies’ shareholders, which could be distributed to investors as a dividend or be reinvested into their businesses. Given Baidu’s currently high cash position, we believe the company would likely decide to distribute the windfall from the IPO as a dividend.

Scenario #3: Alibaba could decide not to follow in Baidu’s footsteps and keep its T-head unit wholly owned inside the company. This would limit the increase in its share price, though market sentiment around chip IPOs stemming from Baidu’s spinoff may potentially raise Alibaba’s valuation if its revenue share increases. The company could still decide to pursue an internal restructuring, thereby calling out T-Head as a key component of its business and breaking out its revenue consistently. Alibaba pursued a similar strategy in 2023 by breaking itself into six businesses without any spin-offs. This may have triggered investors to look at the company through the lens of an SOTP analysis. Alibaba’s stock has risen over 80% since that restructuring.²

Conclusion

Alibaba and Baidu are full-stack AI value generators if you include their chipmaking units in a holistic analysis of their businesses. A sum of the parts of analysis suggests that these units are undervalued relative to comparable businesses. Spinning off their chipmaking units, or at least forcing the market to value them separately, could generate significan shareholder value.

Citations:

- Butts, Dylan. "Baidu's semiconductor unit Kunlunxin files for Hong Kong listing amid AI chip boom in China," CNBC. January 2, 2026.

- Reuters. "Waymo Seeking About $16 Billion near $110 Billion Valuation, Bloomberg News Reports," Reuters. January 31, 2026.

- Company report as of 12/31/2025.

- "PROPOSED SPIN-OFF AND SEPARATE LISTING OF JD LOGISTICS INC. ON THE MAIN BOARD OF THE STOCK EXCHANGE OF HONG KONG LIMITED," JD.com Inc., HKEX News. February 16, 2021.