Electric Vehicles ETF: Metals Prices Signal Potential Opportunity For KARS

By  Henry Greene

Henry Greene

Demand for lithium and other electrification metals, such as nickel, cobalt, copper, and graphite, is rising as electric vehicles (EVs) and energy storage systems are scaling rapidly, accelerated by the oil price shock earlier this year. We believe electrification has moved from an environmental conservation project to an energy security imperative, which could benefit our electric vehicles ETF, the KraneShares Electric Vehicles & Future Mobility Index ETF.

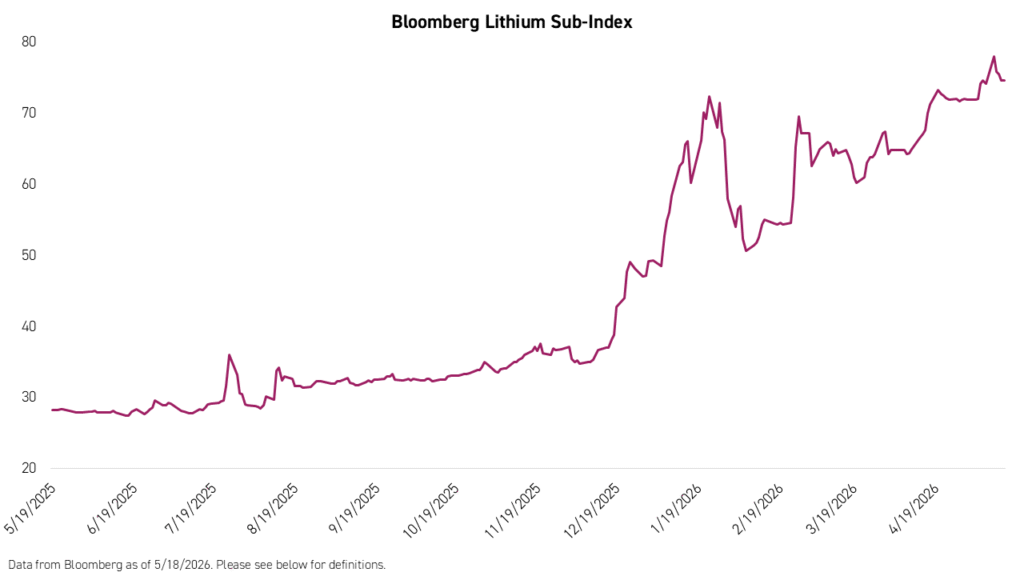

This new paradigm has led to a sharp increase in the prices of many of the metals required for electrification, such as lithium.

However, even as electric vehicle sales continue to reach new highs, manufacturers’ share prices have experienced headwinds, including tariffs, the expiration of subsidies and tax incentives in certain markets, and overcapacity, which has lowered profit margins.

This illustrates that components of the electrification ecosystem do not always move in lockstep. Moreover, even a significant macroeconomic event that could benefit the industry, such as a sudden, unexpected surge in oil prices, does not necessarily lift all boats.

As a diversified* basket of EV makers, component technology producers, and materials suppliers, KARS could benefit from the continued strong performance of metals suppliers and a potential rebound in the share prices of key EV manufacturers.

We believe the surge in demand for electrification metals, rare earths, and other critical materials over the past year has been driven not only by EVs themselves, but also energy storage needs, policy commitments, supply constraints, and broader electrification trends.

EVs: Demand Continues to Rise

Global electric vehicle (EV) sales keep reaching new highs, with more than 20 million units expected in 2025, and batteries now account for nearly 90% of lithium demand, up from about 64% in 2020.1

Many automakers have committed to lineups that are mostly or fully electric by 2030 to 2035.2 This effectively hard-wires multi‑year growth in demand for battery metals like lithium, nickel, cobalt, and copper, even if year-to-year demand remains volatile.

Grid & Stationary Energy Storage

Grid‑scale battery storage exceeded 90 gigawatt-hour (GWh) installations in 2024, and forecasts from sources like Bloomberg New Energy Finance (NEF) point to storage demand compounding at 30% or more through the back half of this decade.3

As more wind and solar are added to power systems, storage is needed to balance intermittency, which pulls in large additional volumes of lithium, plus copper and other conductors for associated grid build‑out.

Contemporary Amperex Technology (CATL), the world’s largest battery maker and a top KARS holding (4.39% as of 3/31/2026), is already contributing to energy storage projects in the United States alongside its partner, the Ford Motor Company.

Policy & Decarbonization Commitments

Industrial policies such as the European Union’s “Fit for 55” and China’s ongoing EV and battery subsidies provide multi‑year visibility for battery and EV manufacturing, anchoring demand for lithium and other critical minerals well beyond short‑term price cycles.

Meanwhile, international energy agencies like the International Energy Agency (IEA) and International Renewable Energy Agency (IRENA) project lithium demand from clean energy technologies to more than triple by 2030.4

Structural Underinvestment & Supply Constraints

Goldman Sachs predicts an 8.2 million metric ton gap in copper demand that will need to be overcome by 20305 if current expectations for electrification are to be met. Historically, under-investing in new projects raises the risk that demand growth will outpace supply.

Meanwhile, the Iran War has highlighted just how fragile supply chains for critical industrial inputs can be, raising awareness among corporations and governments alike.

Broader Electrification & Technology Trends

Beyond EVs, the rising penetration of consumer electronics, data centers, and industrial automation also adds to demand for high‑performance batteries and conductors. This could incrementally lift the consumption of lithium, copper, and related metals.

Meanwhile, geopolitical and supply‑chain security concerns are prompting countries to localize critical mineral supply. This is triggering more projects and locking in higher baseline demand as strategic stockpiles and redundant capacity are built.

Ecosystem Exposure Through KARS

Investors can access the materials companies benefiting from these trends, but also the electric vehicle manufacturers driving demand through our electric vehicles ETF, the KraneShares Global Electric Vehicles & Future Mobility Index ETF (Ticker: KARS).

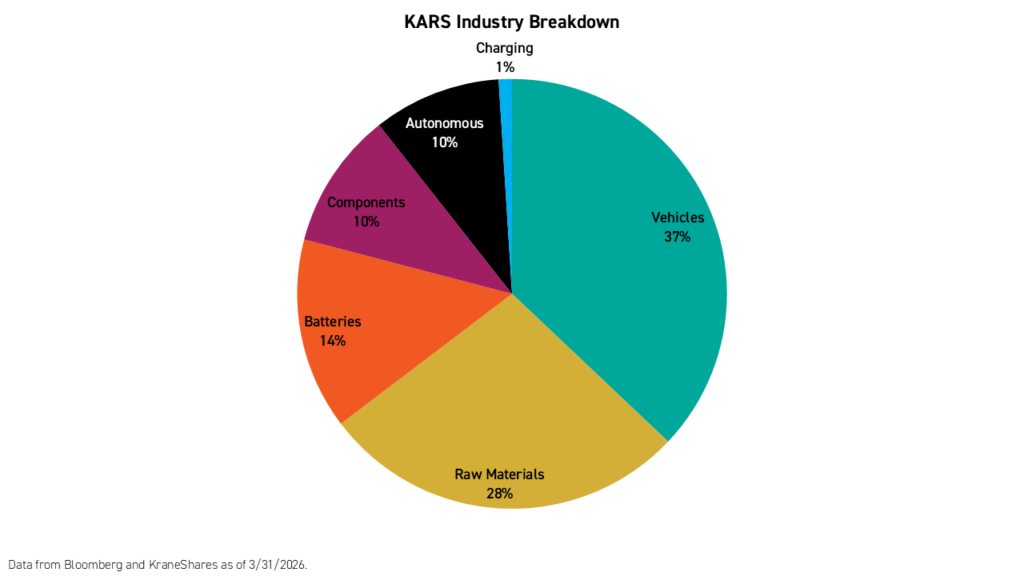

KARS is composed of 28% raw-materials companies that deal in lithium, copper, and other key inputs.

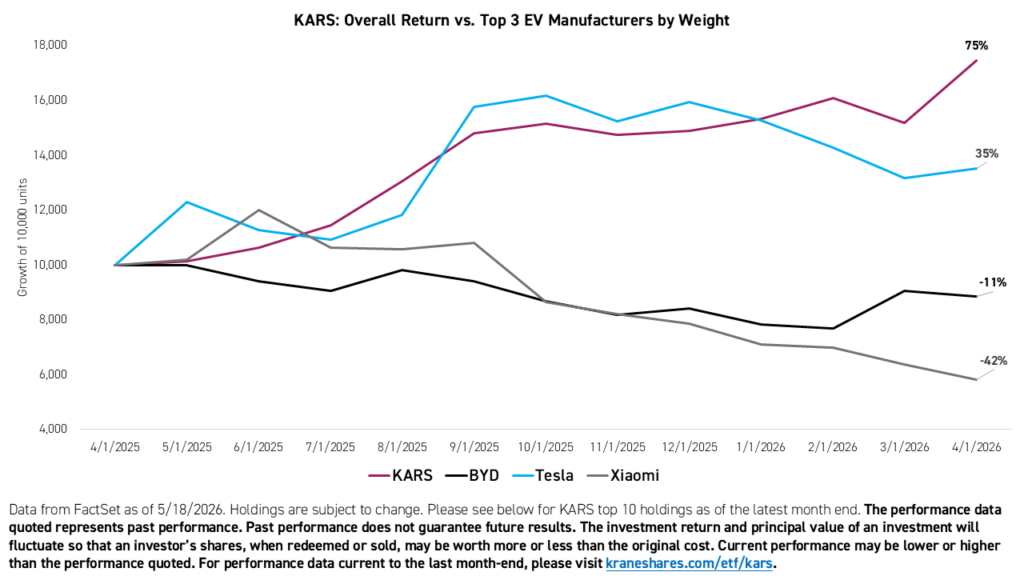

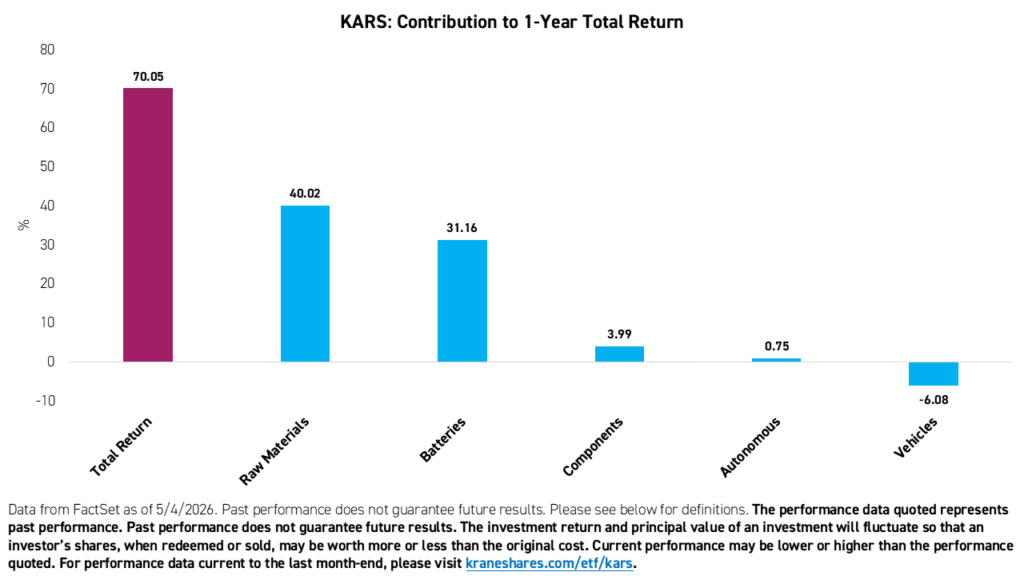

Over the past year, raw materials and charging stocks have contributed the most to the Fund’s total return. Meanwhile, vehicle stocks have come under pressure within the portfolio.

Conclusion

Demand for lithium and other electrification materials has risen steadily over the past year, driven by expectations that the oil price shock will accelerate electrification trends already in motion. Despite continued strong demand, many vehicle manufacturers have seen their share prices decline over this period. KARS provides exposure to a basket of vehicle manufacturers and metals and materials producers, capturing potential opportunities across the electric vehicle ecosystem and providing a potential hedge against oil-related risks.

For KARS standard performance, top 10 holdings, risks, and other fund information, please click here.

|

Top 10 Holdings as of 04/30/2026 Excluding cash. Holdings are subject to change. |

Ticker | % |

|---|---|---|

| STMICROELECTRONICS NV | STMPA | 5.59 |

| Panasonic Holdings Corporation | 6752 | 4.54 |

| BYD CO LTD -A | 002594 | 4.25 |

| CONTEMPORARY AMPEREX TECHN-A | 300750 | 4.20 |

| ALBEMARLE CORP | ALB | 4.20 |

| SAMSUNG SDI CO LTD | 006400 | 3.99 |

| TESLA INC | TSLA | 3.40 |

| BAYERISCHE MOTOREN WERKE AG | BMW | 3.06 |

| GEELY AUTOMOBILE HOLDINGS LT | 175 | 3.02 |

| XIAOMI CORP-CLASS B | 1810 | 2.92 |

Citations:

- Jarber, Samir. “What’s Driving Lithium Demand in 2025 and Beyond?”, Metals Hub. August 18, 2025.

- Craig, Matthew. “Lithium remains key in the energy revolution as a supply deficit looms,” The Market Bull. February 7, 2025.

- Bloomberg New Energy Finance as of 12/31/2025.

- Data from International Energy Agency (IEA) and International Renewable Energy Agency (IRENA) as of 12/31/2025.

- Zadeh, Jonah. “Decarbonisation in Mining 2024/25: Strategies, Challenges, and Opportunities,” March 14, 2025.