KWEB Earnings & The AI Trade in China ETFs

By  Henry Greene

Henry Greene

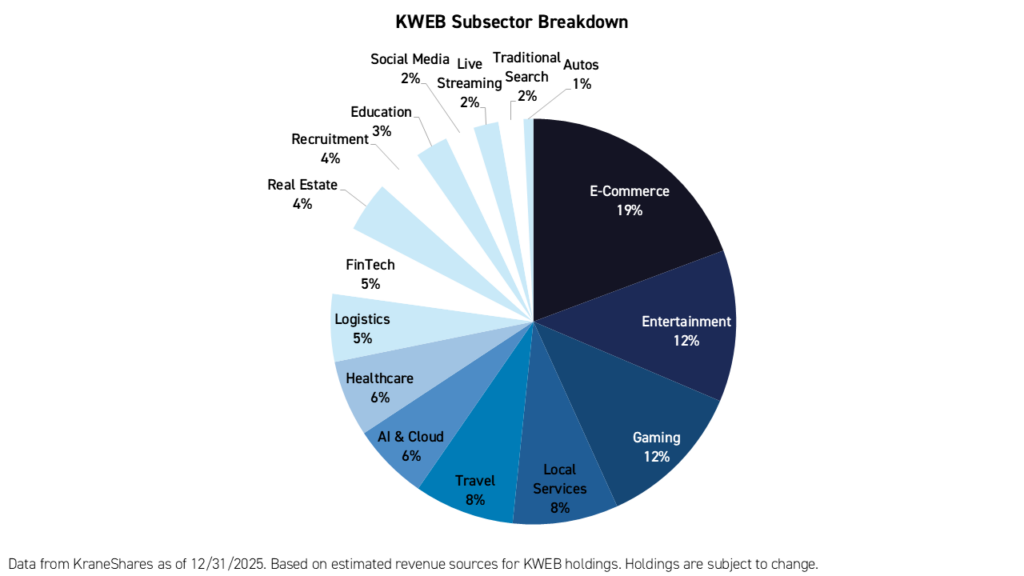

AI has been a growing contributor to revenue for China's internet companies. The KraneShares CSI China Internet ETF (Ticker: KWEB) is a China AI ETF that provides exposure to the major players in China's internet and AI ecosystem.

The companies in KWEB increased their total revenue attributable to cloud computing and AI services by 13% year-over-year in the fourth quarter of 2025.1 At current levels, we estimate that the annual revenue earned from cloud computing and AI services in the China AI ETF could reach over $50 billion in 2026.1

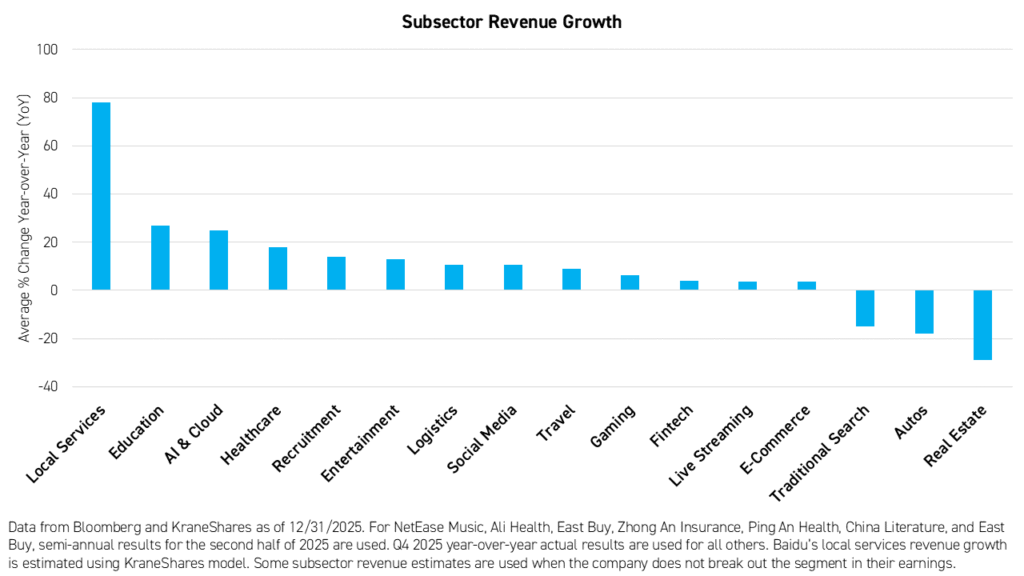

Below, we summarize the key developments in each of the subsectors within KWEB in the fourth quarter of 2025.

AI & Cloud

Revenues increased 25%. Tencent made WeChat and QQ compatible with the popular international agentic AI platform Open Claw. Meanwhile, Alibaba released the latest version of its Qwen large language model (LLM). Alibaba also projected cloud revenues doubling every year over the next five years. And, its chipmaking unit T-Head is on track to reach RMB 10 billion in annual revenue. That would bring T-Head close to the annual revenue of Cambricon, a leading China-based fabless chipmaker. OpenAI announced it would be closing its Sora video creation platform, effectively ceding the space to Kuaishou’s Kling AI globally. Kling AI had already achieved monthly active users (MAUs) of nearly 12 million, while Sora had only reached 2 to 4 million MAUs.

Local Services

Local Services revenues for KWEB companies increased 78% in the fourth quarter. Strong consumer subsidy spending from JD, Meituan, and Alibaba ensured consistent user retention and steady volume increases, while weighing on profitability. JD, in particular, tripled revenue from JD Now, a specialized service offering delivery of various consumer goods within 30 minutes to urban consumers. However, growth could slow as the platforms have agreed to reduce spending on promotions and prioritize profitability.

Education

Education platform TAL increased revenue by 27%. TAL reported strong growth in its online and its offline tutoring programs. Also, its Singles’ Day promotion season was successful. TAL also unveiled a new learning device for children ages six to eleven at the 2026 Consumer Electronics Show (CES) in Las Vegas, where it received a “CES Picks” award.

Healthcare

Healthcare platforms JD Health and Ali Health reported results for the second half of 2025. Their revenue increaseed 18%, on average. Ali Health beat estimates on revenue and net income for the full year of 2025. Both platforms benefited from a shift in strategy by many pharmaceutical companies from hospital procurement to direct online sales. This shift has been partly driven by policy reforms in recent years.

Recruitment

Kanzhun, which operates the popular “BOSS Zhipin” job search app, increased revenue 14% in the fourth quarter. Management noted strong demand for employment driven by Lunar New Year holiday consumption trends. Meanwhile, blue-collar jobs outperformed placements for white-collar roles.

Entertainment

Entertainment revenues increased 13%. Bilibili and Tencent Music benefited from improved monetization for their premium subscribers.

Logistics

Logistics revenues increased 11%. JD Logistics, a logistics spinoff from JD.com benefited from increased demand from its parent platform. Meanwhile, Full Truck Alliance, sometimes referred to as the “Uber of trucking”, increased revenue and profitability in the fourth quarter. Full Truck benefited from efforts to overhaul its model to favor commission-based orders, rather than wholesale future capacity sales. The company also reported a 12% increase in completed orders.

Social Media

Social Media revenues increased 10% on average, led by Tencent’s WeChat, which benefited from a pickup in advertising spending driven by new AI tools. Meanwhile, despite seeing more tepid growth than WeChat, Weibo noted strong growth in the E-Commerce and auto segments of its social media advertising sales and expects this momentum to continue throughout 2026.

Travel

Travel revenues increased 9%. High demand for domestic travel among China’s consumers, especially for experience-based bookings, led to decent growth for travel booking platforms. Trip.com saw strong growth in both its overseas business and domestic China travel. Gaming revenues increased 6%. However, key game makers within KWEB delivered highly variable results. Tencent, the growth leader for the quarter, saw international games growth outpace domestic games growth by a significant margin, on the back of popular international titles like PUBG. Meanwhile, NetEase’s revenue was lower than expected in the fourth quarter as demand for legacy titles was subdued. Finally, XD turned profitable thanks to improving economics for its game-sharing platform, known as TapTap, in China.

E-Commerce

E-Commerce revenues increased a modest 4%, challenged by a high base in the final quarter of 2025. Trade-in subsidy usage has declined since then, as many households have already taken advantage of the program by upgrading home appliances and other large items. Meanwhile, core domestic commerce growth was sluggish for both JD.com and Alibaba, though PDD Holdings experienced strong growth in both domestic and international commerce thanks to an advertising push and expansion into lower-tier cities and rural areas.

FinTech

FinTech revenues also increased 4%, led by insurance platform Zhong An, which benefited from growth in new categories such as pet and drone insurance. Meanwhile, growth was challenged for consumer lending platforms like Qfin, which faced regulatory caps on interest rates and new loan origination rules that tightened liquidity. Meanwhile, Tencent’s WeChat Pay continued to experience strong growth.

Live Streaming

Live Streaming revenues increased 4%. East Buy rebounded from the loss of some celebrity key opinion leaders (KOLs) in 2024. Meanwhile, Kuaishou experienced a slight decrease in its live streaming revenue, but reported upgrades to its live streaming platform such as the introduction of multi-host live streaming events as well as the integration of live streamed products into AI suggestion models.

Traditional Search

Traditional Search revenue for Baidu has hit record lows, down 15%, as AI-powered search continues to take market share. This led the company’s CEO to effectively declare that AI has become the “new core” of Baidu during the company’s earnings call.

Autos

Auto platform Autohome reported an -18% decrease in revenue, driven by lower advertising spending from internal combustion engine (ICE) automakers. Meanwhile, the platform faced strong competition from short-video platforms for advertising spending from electric vehicle (EV) brands. Lead generation and customer support services for dealers were more resilient but did not offset declines in the company’s core businesses.

Real Estate

Real Estate platform KE Holdings reported a 29% decline in revenue, which its management attributed to a high base effect for the new home transactions in the final quarter of 2025. Overall, price recovery in China’s residential real estate market remains gradual.

For KWEB top 10 holdings, risks, and other fund information, please click here.

Citations:

- Data and estimate from Bloomberg and KraneShares as of 3/31/2026.