Breaking Down Securities Lending Benefits to ETF Investors

The rapid adoption of exchange-traded funds (ETFs) over the last two and a half decades has been an incredible phenomenon. With a wide-range of ETFs available, picking an ETF that will meet investment goals requires in-depth analysis. Generally, ETF due diligence focuses on the expense ratio, portfolio composition, performance, AUM and average daily trading volume. Although these are key considerations, an ETF’s securities lending program can be a key differentiator. Despite potential benefits for investors, namely an additional revenue stream, securities lending is often overlooked as an important element of the due diligence process.

Article Summary:

- What is securities lending

- How does securities lending work

- What are the benefits to ETF investors

- Review of securities lending regulation

- What are the potential risks of securities lending

What is Securities Lending?

In order for an investor to borrow a stock, they need to acquire it from a current shareholder. ETFs make good supply side candidates for securities lending given that they tend to have a portfolio of large positions that are liquid. The individual stocks within an ETF are usually borrowed through an intermediary called a securities lending agent (often the ETF’s custodian). The lending agent negotiates terms and arranges the loan with counterparties on behalf of the ETF.

In securities lending the lending yield (how much it costs to borrow securities) is driven by demand. The more market demand there is to borrow a stock, the more a borrower is willing to pay. Similarly, the less demand, the lower the lending yield. A common misconception is that borrowers are always investors who wish to short a security because they believe its value will fall. This is not necessarily the case. Other reasons that securities are borrowed include the clearance of trade fails, the execution of certain arbitrage strategies, and options market makers as well as ETFs hedging their positions. When an ETF lends a stock, they receive collateral in exchange. The amount of collateral changes based on the price of the borrowed securities. If the value of the underlying borrowed security goes up, the borrower will have to deliver more collateral, and vice versa. Regardless of a security being on loan the ETFs value includes that of the underlying security.

Benefits of Securities Lending for Investors

The benefit to ETFs that utilize securities lending is an additional income stream. The income earned from securities lending is usually estimated and accrued daily into the ETFs NAV and is distributed on monthly basis. Securities lending tends to increase when an ETF’s underlying asset class, sector or market is out favor or lacks liquidity. From a strictly GAAP (Generally Accepted Accounting Principles) standpoint, securities lending income is classified as its own line item of investment income and is not used to directly offset management fees on the income statement. However, within the ETF industry, it is common practice to view ETF ownership as a balance sheet, juxtaposing securities lending income against fund management fees. Viewed this way, securities lending income may improve the cost of ETF ownership, compared to the same strategy without a securities lending component. While securities lending revenue can vary day to day, an investor can find the management fee and historic data on securities lending income in an ETFs’ semi-annual and annual reports.

To give an example from KraneShares Semi-Annual Report from September 30, 2018 KWEB’s securities lending income was $3,252,945 and securities lending fees totaled $322,258. KraneShares management fee during this time period was $4,967,547. After deducting lending fees from the lending income, the total lending income ($2,930,687) offsets almost 60% of management fees.

Regulation

The SEC determines the rules governing securities lending for ETFs. The maximum percentage of the portfolio that can be lent out is one third¹. The SEC also regulates the amount of collateral received and what can be used as collateral. Today, only U.S. Treasury bills /agencies and cash can be taken as collateral. Cash collateral is usually invested in a government money market fund, a 2a-7 prime money market fund and, and/or repurchase agreements. For U.S. securities the borrower has to provide collateral worth 102% of the security's value. For non-U.S. securities, the borrower has to provide collateral worth 105% of the security’s value. As previously noted, the amount of collateral is adjusted daily based on the securities rising or falling in value. These safeguards are in place to protect the ETF’s shareholders.

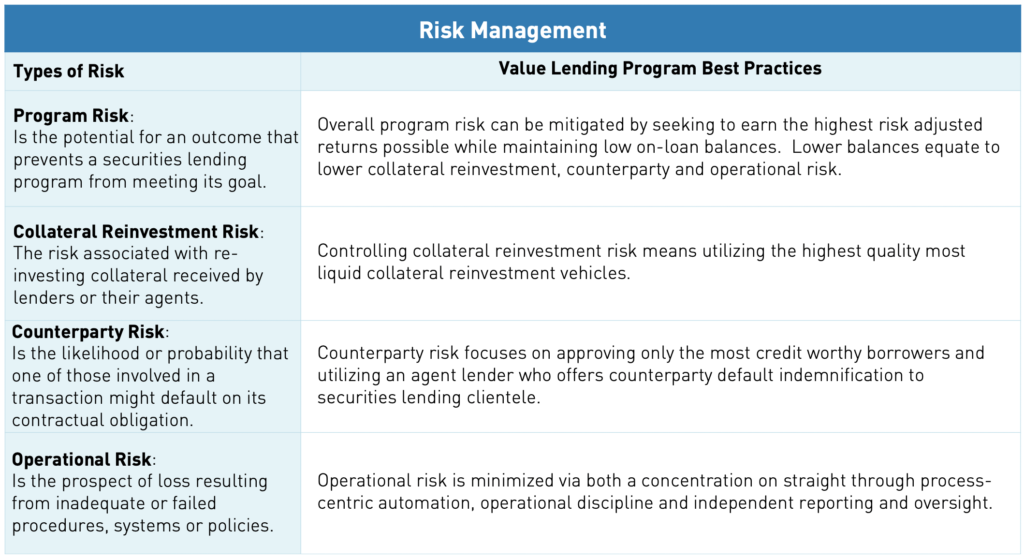

Risk Overview

As with all investments understanding risk factors is a key part of the equation. We believe our best tool to mitigate risk is performing due diligence and analysis before investment decisions are made. KraneShares partners with Brown Brothers Harriman (our lending agent and custodian) to address four key risk components: program risk, collateral reinvestment, counterparty risk and operational risk.

Given the benefits of securities lending, we encourage investors to incorporate this data point into their due diligence process and further examine the securities lending practices of the ETFs that they are considering. The income stream from securities lending can produce a meaningful reduction in the cost of owning an ETF.