Revisiting Hong Kong: Optimism Still Improving Even As Rally Gets Tested

By Brendan Ahern, KraneShares CIO

When I visited Hong Kong in December of 2023, the city was full of energy with the usual traffic and frantic shoppers preparing for the Christmas and New Year’s holidays. However, investors and trading desks were feeling the full brunt of China’s three-year bear market. The effect of the market’s daily grind lower was palatable. Trading volumes contracted, initial public offerings (IPOs) were shelved, and mergers and acquisitions were put on hold. Sparks of optimism were abruptly snuffed out as the rally following the removal of China’s zero COVID policy proved unsustainable. Although December’s extreme pessimism felt like a contrarian indicator, the market had one last plunge in store, which occurred in January 2024.

The final liquidation event was triggered by the overcrowding in mainland small caps in what has been called China’s “quant quake” and the subsequent meltdown of derivative instruments, ironically called “snowballs”. The forced liquidation event paired with very light investor positioning sent Chinese equities down on the proverbial elevator.

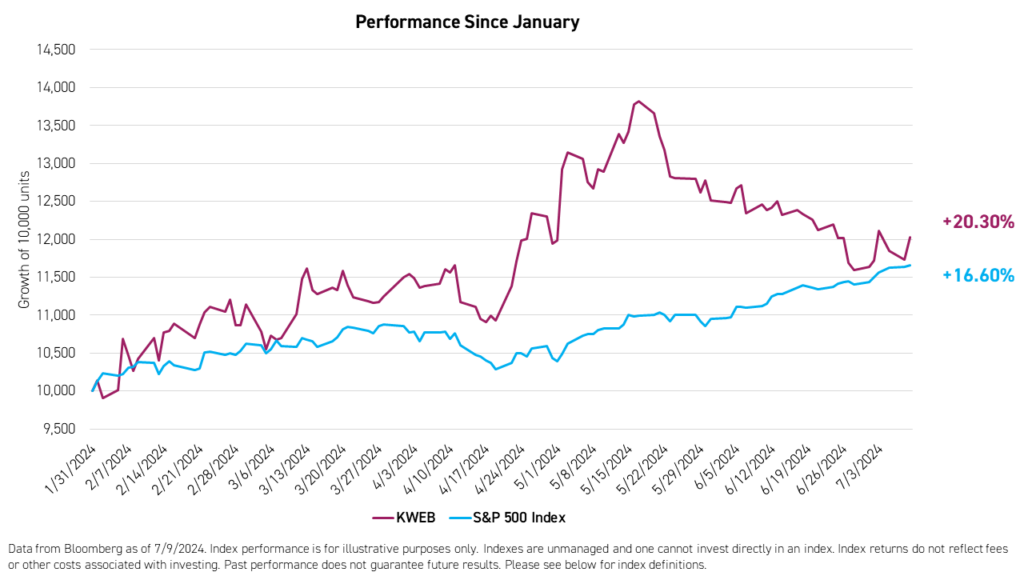

In a previous article, we provided five reasons why the recent rally in China’s overall stock market may be different from the past. Although we have seen a pullback from recent highs, we still see strong support for the upswing since January based on the fundamental reasons we outlined, especially for Hong Kong-listed internet stocks. The KraneShares CSI China Internet ETF (Ticker: KWEB) continues to outperform the S&P 500 since the end of January, despite the recent pullback.

The performance data quoted represents past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed or sold, may be worth more or less than the original cost. Current performance may be lower or higher than the performance quoted. For performance data current to the last month-end, please visit our website by clicking here.

My June trip to Hong Kong was visually the same with busy streets, crowded restaurants and busy malls. However, what had changed from December was the mood of local investors. So, what was on the horizon that had them excited?

The 6.18 E-Commerce Sales Festival Shows Spending Hibernation is Thawing.

While the Singles’ Day (November 11th) E-Commerce is widely known today, the 6.18 (June 18th) E-Commerce event is not as well known outside of China. However, the 6.18 deal bonanza is just as impactful for merchants, consumers, and of course platforms.

JD.com started its pre-sales on May 31st at 8 pm. The company reported that “brands, including Apple, Midea, Haier, Xiaomi, China Gold, Huawei, Little Swan, Gree, Hisense, TCL and others saw transaction volumes surprass RMB 100 million just in the first day. In the first four hours of the sales event, foreign brands were also in the spotlight. L’Occitane and Pampers both saw event sales increase +600% year-over-year (YoY) in those crucial first four hours. Also seeing progress were brands including Nike, whose sales were up +100% YoY, Loewe, whose sales were up +250% YoY, Tiffany & Co., whose sales were up +100% YoY, and Alexander Wang, whose sales were up +450% YoY.1

Alibaba, which kicked off its mid-summer promotions earlier than JD, reported that 365 brands crossed RMB 100 million ($14.1 million) in gross merchandise value (GMV) during the festival, while 216 products alone contributed over RMB 10 million in GMV. Alibaba’s loyalty program campaign also appears to have paid off with a +40% year-over-year increase versus 2023. The number of new “88VIP” users added during the sales festival this year was +65% more than last year.2

The 6.18 Sales Festival results reflect strong momentum since online retail sales increased by +12.4% in May, accounting for 24.7% of total retail sales of consumer goods.3

There has been a change in the tone and tenor of China’s leaders toward foreign business and investment.

Back in January, the Vice Chairman of the China Securities Regulatory Commission (CSRC), which is China’s version of the SEC, said that Americans tend to be direct while Chinese culture leans toward the use of more subtle messaging. Keen observers may have noticed the following:

- President Xi goes to San Francisco to meet President Biden at the APEC meetings.

- President Xi decides to have dinner with US corporate executives at APEC.

- APEC cooperation outcomes include fentanyl pre-cursors and military dialogue.

- China approves Broadcom's acquisition of VMware.4

- China re-approves the Boeing 737 MAX for flights in China.5

- San Diego, San Francisco and, most importantly, Washington, D.C. will receive pandas following the “retirement” of previous pandas.

July’s “Third Plenum” economic meetings may indicate intensified stimulus measures.

China’s government has not deployed the preverbal “policy bazooka” having witnessed the increase in debt and inflationary consequence of loose Western countries’ monetary policies post COVID. However, incremental policy support has occurred. July's "Third Plenum", a government economic meeting attended by President Xi and senior leadership, will provide investors the opportunity to better understand the direction of policy. In speaking of the upcoming event, President Xi stated “"We are planning and implementing a series of significant measures to comprehensively deepen reform." 6 While investors’ expectations remain muted, we anticipate policy support amplification to increase with an emphasis on real estate and domestic consumption.

Chinese firms are on a stock buying spree.

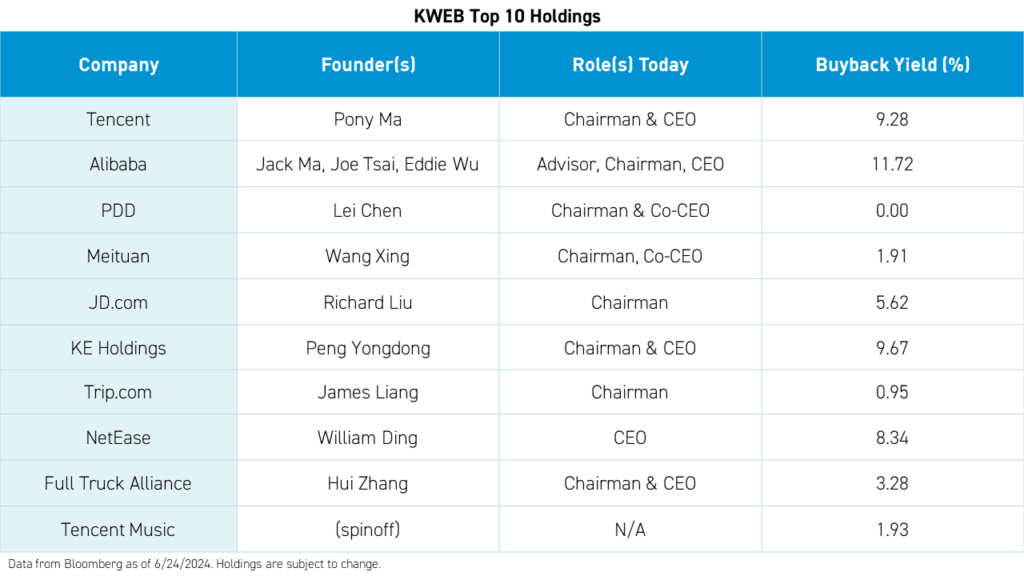

Another positive catalyst is that Chinese companies are increasing their stock buybacks and dividends, which is a strong indication of their overall financial health and shareholder focus. Brilliance Automotive impressed the market when it announced an HKD 4.60 dividend with a share price of HKD 6.00. Although Brilliance is an outlier, it is not alone in increasing its dividends. The CSRC’s “Nine Measures” to stabilize the capital markets, released in April, include encouraging more companies to initiate or increase dividend payments and buy back stock.7 In fact, companies’ stock will be assigned a warning label for failure to pay out a certain portion of profits. The companies held by the KraneShares CSI China Internet ETF (ticker KWEB) are predominantly managed by their founders. We believe this “sweat equity” is an underappreciated characteristic of technology entrepreneurs who have a vested interest in their company’s outlook and stock price.

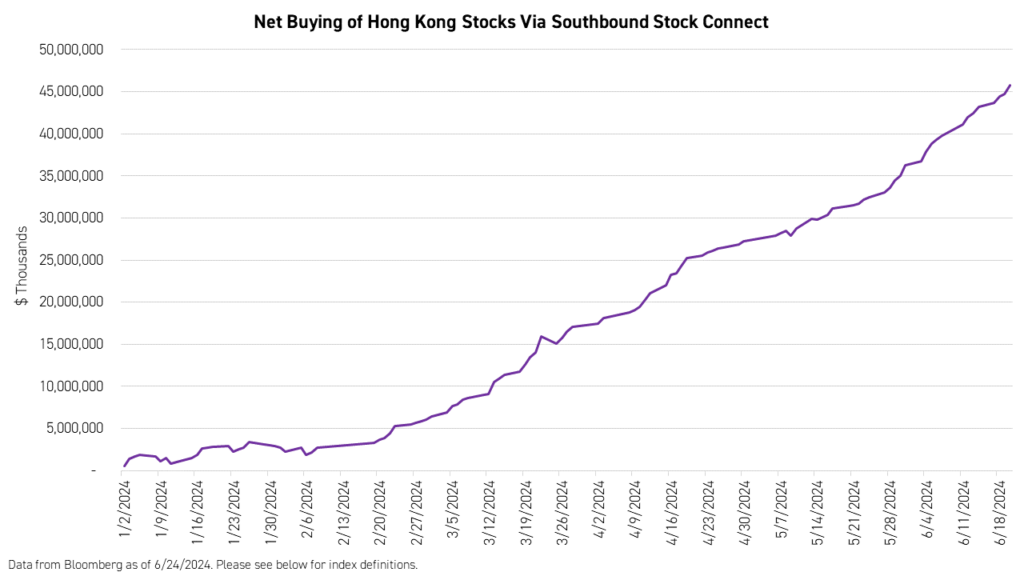

Mainland investors are buying Hong Kong stocks in size and Alibaba could soon be among their purchases.

Southbound Stock Connect allows mainland Chinese investors to buy Hong Kong listed stocks. Year to date, net buying, buys minus sells, has exceeded net buying in 2023. This is a clear sign, in our opinion, that Mainland investors are noticing the valuation opportunity in many Hong Kong-listed stocks.

Another potential catalyst is Alibaba’s recent filing to make Hong Kong share class its primary listing. This is important because with Hong Kong as its primary listing venue, Alibaba would become eligible for Southbound Stock Connect, which is the mutual market access program that allows Mainland investors to trade Hong Kong-listed stocks and ETFs. We believe this could occur as soon as September. What is the potential inflow opportunity for Alibaba? Southbound-available Tencent and Meituan are 9% and 13% owned by Mainland investors through Southbound Stock Connect, respectively.8

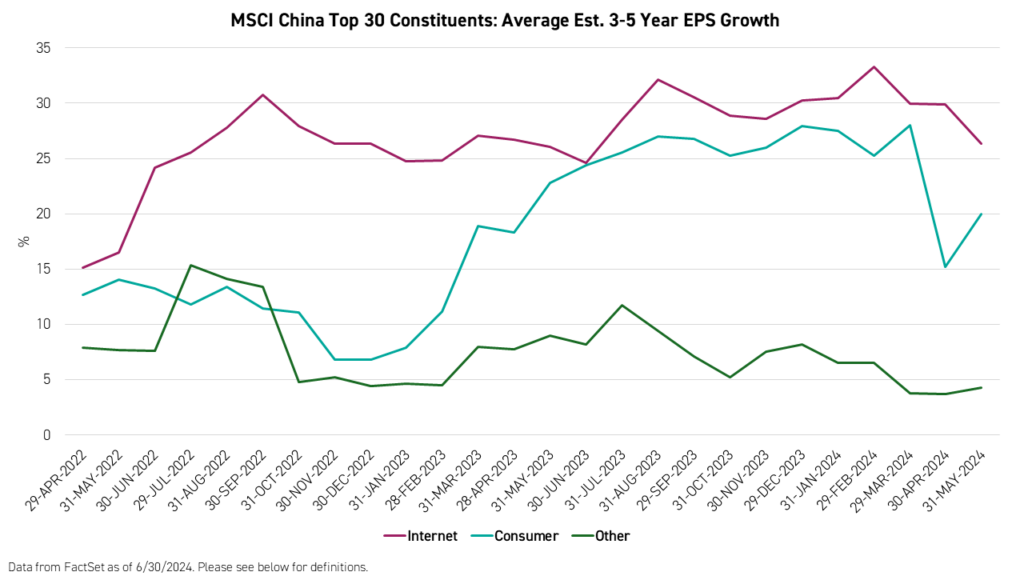

Internet stocks, primarily Hong Kong-listed, are earnings leaders in China.

Within the top 20 constituents of the MSCI China Index, internet stocks are expected to grow their earnings per share (EPS) at a 30% faster rate over the long-term versus consumer-only names and five times the rate of stocks from companies in other industries.

Conclusion

I was pleased to return to Hong Kong last month and experienced renewed optimism among investors and trading desks. While we believe the fundamental support for the rally in China’s stock market overall remains intact, Hong Kong-listed, internet stocks might be particularly attractive and poised for further gains because of recent better-than-expected online shopping trends among consumers, outsized share buyback and dividend policies, and strong fundamentals relative to other industries in China, among other potential catalysts, including July's "Third Plenum" important government meetings.

For KWEB standard performance, top 10 holdings, risks, and other fund information, please click here.

Citations:

- Data from Alibaba as of 6/18/2024

- Data from JD.com as of 6/1/2024

- Data from the National Bureau of Statistics of China as of 5/31/2024.

- "Tech war: China approves Broadcom-VMware merger with conditions, in sign of thaw with US," South China Morning Post. November 22, 2023.

- Mondal, Pollock. "Boeing set to resume operations at Zhoushan facility amid thriving Chinese aviation market," Associated Press. November 16, 2023.

- "China vows reforms at long delayed party conclave amid challenging economy," Reuters. April 30, 2024.

- Data from Wind as of 6/20/2024.

- CSRC as of 4/30/2024.

Definitions:

S&P 500 Index: The S&P 500 is a stock market index tracking the stock performance of 500 of the largest companies listed on stock exchanges in the United States.

Nasdaq 100 Index: The Nasdaq 100 Index includes 100 of the largest domestic and international non-financial companies listed on the Nasdaq Stock Market based on market capitalization. The index reflects companies across major industry groups including computer hardware and software, telecommunications, retail/wholesale, and biotechnology. The index was launched on February 1, 1985.

MSCI China Index: The MSCI China Index captures large and mid-cap representation across China A shares, H shares, B shares, Red chips, P chips and foreign listings (e.g. ADRs). With 703 constituents, the index covers about 85% of this China equity universe. Currently, the index includes Large Cap A and Mid-Cap A-shares represented at 20% of their free float adjusted market capitalization. The index was launched on October 31, 1995.

Average Est. 3-5 Year EPS Growth: The expected annualized growth rate in earnings per share of a company over the long term (3 or 5 years, depending estimate availability). A simple average is used for index constituents.

Share Buyback Yield: The value of the outstanding purchases in a company's current share repurchase plan as a percentage of the company's current free-float market capitalization.

Southbound Stock Connect: A mutual market access program that allows buyers located in Mainland China to purchase certain stocks listed in Hong Kong.