While “Delisting” Gets Headlines, The SEC Proposes Orderly Solution

On Wednesday, the House passed Bill S.945 The Holding Foreign Companies Accountable Act, which will require US regulators to review the audit books of US-listed Chinese companies or face delisting if they do not come into compliance within three years. While headlines around this bill have emphasized the potential delisting component, they have not highlighted the substantial progress the Securities and Exchange Commission (SEC) has made in providing a framework for resolving the issue.

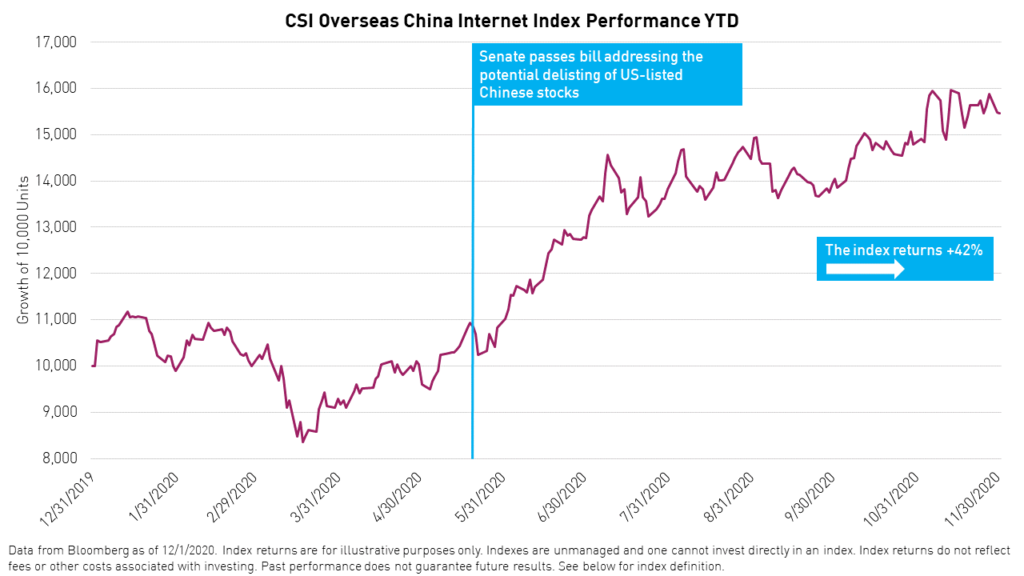

US-listings of major Chinese internet companies came under pressure when the bill passed in the senate on May 20th, but quickly reversed course. The CSI Overseas China Internet Index has returned +42% since the senate passage.1

Before the vote, California Rep. Brad Sherman remarked that the legislation's intent is to provide the SEC with the discretionary power to bring companies into compliance with the law. It is critical to note that enforcement of the law will be handled by the SEC, which is likely to follow the guidelines outlined previously in the President's Working Group on Financial Markets. The SEC's proposal would involve having US-listed Chinese companies' audits reviewed by firms located in jurisdictions that are accessible to the Public Company Accounting Oversight Board (PCAOB), such as the US. The PCAOB is a US regulator that sets accounting and reporting standards for all publicly-traded companies listed in the US.

The vast majority of US-listed Chinese companies are audited by the “Big Four” US accounting firms: PWC, Deloitte, Ernst & Young, and KPMG. While skeptics may question the audit work done by these firms in China, the Big Four apply the same auditing methodology there as they do in the US, Europe, and the rest of the world.

There are over $2 trillion in US savings invested in US-listed Chinese companies such as Alibaba, Baidu, and JD.com. While it is important to ensure these companies are following PCAOB standards, we believe the SEC is likely to do so in a measured and transparent manner to protect shareholders. Furthermore, a wholesale delisting could jeopardize the US’ status as the world’s financial center.

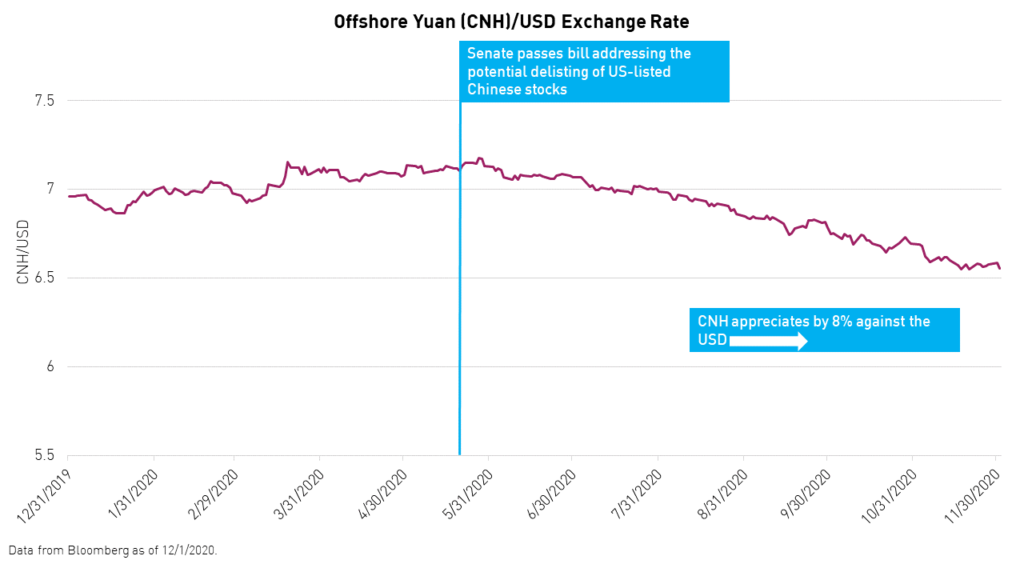

US-listed Chinese companies may see minor pressure in the near term. It is important to note that stock markets are more sensitive to headline risks than currency markets. Time and time again, headlines can lead to stock volatility that that is not reflected in the offshore yuan (CNH)/USD exchange rate. We saw this earlier this year when Bill S.945 passed in the senate.

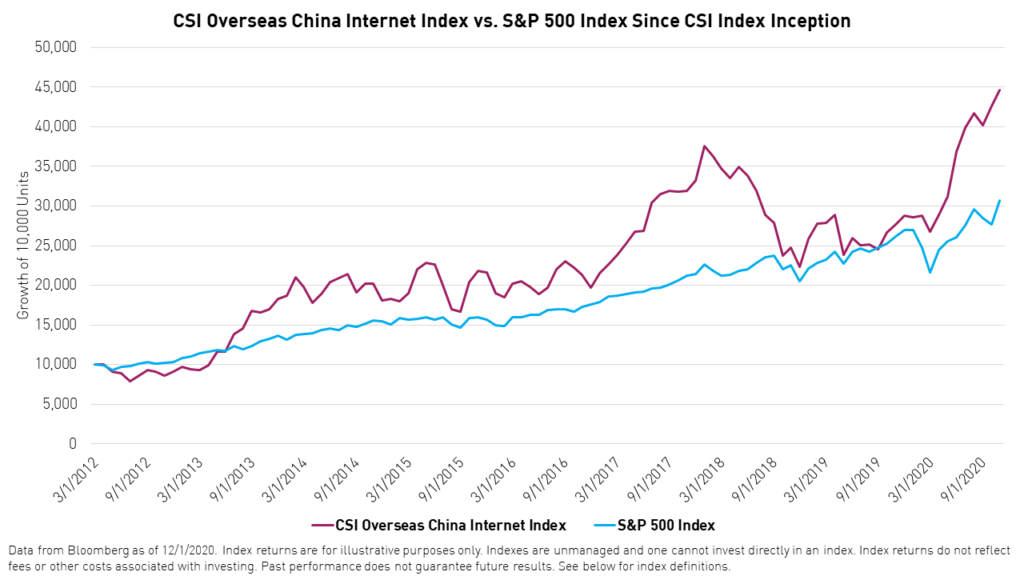

There has been significant emphasis placed on the risk associated with investing in Chinese equities, but little examination of the rewards. We believe the aggregate rewards associated with investing in many of these companies may outweigh the unfortunate “bad apples”. Many would be surprised to learn that NetEase, a US-listed Chinese gaming company that listed back on June 29, 2000, has returned 13,335% since its IPO versus Amazon’s 8,573% return. Alibaba alone has generated hundreds of billions of dollars for its shareholders.1

One reason we are constructive on a positive outcome from Bill S.945 is that numerous new Chinese companies have chosen to list in the US in 2020 including Beike and Lufax Holdings. Clearly these companies and their investment banks believe that de-listing is unlikely.

Additionally, there has been a positive change in Chinese regulators’ tone on this issue. On November 20th, a spokesperson for the China Securities Regulatory Commission (CSRC) was asked by a reporter at a press briefing about this issue. The spokesperson noted that “Chinese companies listed on U.S. stock exchanges follow U.S. laws and regulations for financial reporting and information disclosure. Otherwise, their securities cannot be registered with the U.S. regulatory authorities.” The spokesperson then stated “On 4 August 2020, after thoroughly considering the concerns of the U.S. regulators, the CSRC sent the fourth version of the proposal for joint inspection over audit firms to the U.S. Public Company Accounting Oversight Board (PCAOB). The PCAOB confirmed the receipt of the proposal and suggested that it would examine the proposal in due course. We look forward to starting a meaningful dialogue with the U.S. regulator on the details of the proposal."

If you have any questions about the Bill or KraneShares ETFs, please contact [email protected].

KWEB Holdings Mentioned

- Alibaba (BABA US, 10.71% of KWEB Net Assets as of 9/30/2020)

- Baidu (BIDU US, 4.19% of KWEB Net Assets as of 9/30/2020)

- JD.com (JD US, 7.08% of KWEB Net Assets as of 9/30/2020)

- NetEase (NTES US, 3.94% of KWEB Net Assets as of 9/30/2020)

- Beike (KE US, 3.71% of KWEB Net Assets as of 9/30/2020)

- Lufax Holdings (LU US, 3.95% of KWEB Net Assets as of 9/30/2020)

Citation

- Data from Bloomberg as of 12/1/2020.

Index Definition

CSI Overseas China Internet Index: The CSI Overseas China Internet Index selects overseas listed Chinese Internet companies as the index constituents; the index is weighted by free float market cap. The index can measure the overall performance of overseas listed Chinese Internet companies. The Index is within the scope of the IOSCO Assurance Report as at 30 September 2018. The index was launched on September 20, 2011.

S&P 500 Index: The S&P 500 Index is widely regarded as the best single gauge of large-cap U.S. equities. There is over USD 9.9 trillion indexed or benchmarked to the index, with indexed assets comprising approximately USD 3.4 trillion of this total. The index includes 500 leading companies and covers approximately 80% of available market capitalization. The index was launched on March 4, 1957.

r_us_ks