How Private Equity ETF BUYO May Help Manage AI Software Disruption Risk Versus Illiquid Investments

By Cole Wenner & John Lidington, CFA

To start 2026, there has been ample coverage of the broad selloff in software stocks due to artificial intelligence (‘AI’) disruption risk. This selloff has not only rippled through public markets but also private equity and private credit.

This article will not explore the disruptive threat of AI to specific software products or other parts of the economy, which could be very real for some companies. Rather, it will build on our belief that the sell-off in publicly listed software and software-linked securities may have been broader than warranted.

During this process of figuring out the ultimate winners and losers in the software industry, it is important to keep in mind that indiscriminate selling almost always creates opportunities. Especially for active managers, and particularly for the nimblest active managers.

So, how best to harvest these opportunities?

Public Versus Private Investments During Market Turmoil

In rapidly evolving situations where winners and losers are being identified and priced accordingly in near real-time, should investors feel comfortable being locked into a set of illiquid private software companies that they can’t sell or trim exposure to in the near-term?

Or might it be more prudent to have a liquid, private equity (PE)-mimicking portfolio that invests in publicly listed software companies and can be responsive to the dynamic situations surrounding individual companies, and divest from specific holdings when appropriate? Then, as the dust settles and it becomes clearer which ones may face less disruption risk and thus may be mispriced, a strategy that can be nimble in picking its (re)entry points may allow investors to buy low and potentially capture the recovery more effectively than they can in illiquid private markets.

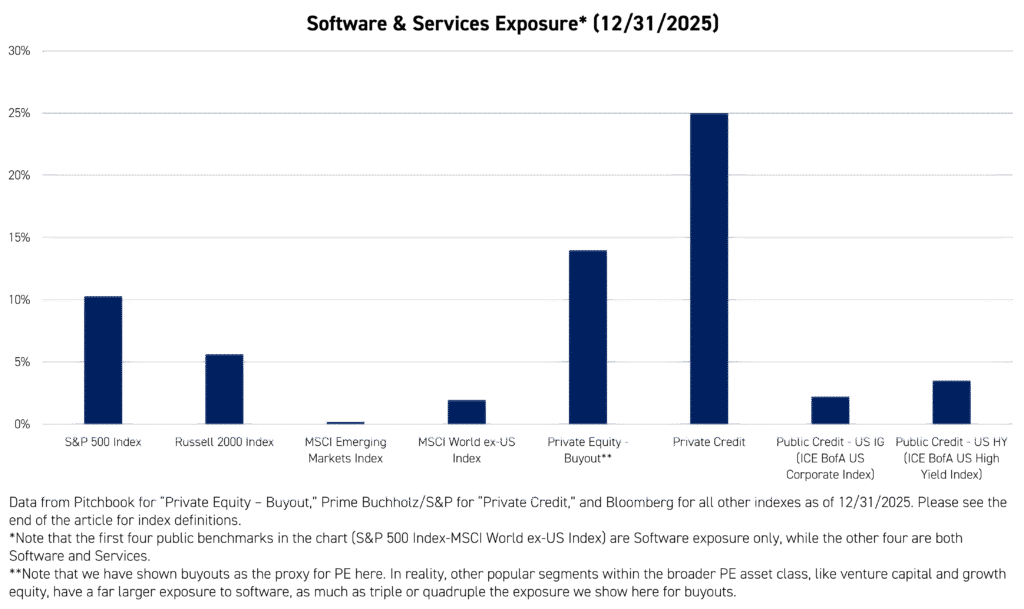

This is the dilemma currently facing many investors, as software is the most dominant industry-level concentration risk in private credit portfolios, at approximately 25% of exposure (possibly higher when different classifications are accounted for), and is a very meaningful exposure within private equity as well at almost 15% of buyout funds.1

The thesis behind investing in software as a service (‘SAAS’) companies was sound at the time the majority of these investments were made (with some deals done during the infancy of or even predating OpenAI, Anthropic, and other popular AI firms), as these companies offered stable and predictable recurring revenue streams, what was thought to be a high cost of replacement, and other attractive features. And this may still be the case for many of these investments. Time will tell.

Meanwhile, public credit and equity indices have had far less direct exposure to the software and services industry than private markets in recent years. That said, there is still ample opportunity for more nimble active managers in public markets to divest from or avoid companies they deem to have a heightened risk of AI-driven disruption.

Along these lines, ‘liquid private equity’ strategies offer the potential to mimic many of PE’s leading return drivers while also featuring the responsiveness and agility to potentially avoid the individual software companies that may face headwinds or even existential threats from AI.

What Liquid Private Equity Strategies Currently Exist?

There are two leading families of liquid private equity strategies worth noting here, both viewed as proxies for PE return drivers but with very different approaches.

- One group seeks to mimic the return profile of PE funds by investing in companies with similar characteristics to PE holdings.

- The other group invests in publicly listed PE/private credit firms as well as Business Development Companies (BDCs) and other firms that are related to but perhaps on the periphery of PE.

It is the first group that we refer to above when saying that they can provide PE-like return drivers and exposures while remaining nimble in terms of selecting winners and losers within the software industry. We believe this is a more direct way to potentially generate PE-like returns.

The second group also presents an interesting case study during the recent software carnage, despite not being software companies. Shares of publicly-listed PE/private credit firms have been selling off, as have many BDCs.

As noted, these two groups are the focus of the second set of exchange-traded funds (ETFs). While this is simply the market pricing in the heightened risk of the underlying assets in these firms’ portfolios and the potential impact on those funds' returns, it highlights the perils of using this narrower set of (largely financial services) securities as a proxy for PE portfolios and performance.

While some PE managers are narrow in their focus on software or broader technology investments, the overall PE asset class is more diversified in its industry exposures, and that diversification is a hallmark of a small cohort of liquid PE strategies that seek to mimic the actual key risks and return drivers of traditional PE, including its industry exposures.*

What to do now?

Does the lack of agility in responding to quickly evolving situations mean you should ignore private markets in wealth portfolios? Probably not, at least as the sole reason to ignore.

But does it mean that you should go in eyes wide open if you are adopting private markets and perhaps consider alternative ways to gain exposure to similar returns if you are not comfortable with some of the risks of traditional private exposure? In our opinion, absolutely!

This will potentially prove to be a Blockbuster moment for a number of software companies, but we believe it is highly improbable that it will be the beginning of the end for all software companies.

What the current software debate illuminates is an important question: when crises arise, how much of your money do you want to be stuck in a slow-moving, illiquid product with limited ability to sell the expected losers?

Private Equity ETF BUYO

For investors seeking exposure to the characteristics of companies targeted by PE, rather than direct ownership of specific private companies, there are now liquid strategies available.

These approaches use quantitative models to identify and mimic the exposures that have historically been observed in private equity investing. KraneShares partnered with Man Group, the world's largest publicly traded hedge fund manager and an alternative investments specialist2, to launch the KraneShares Man Buyout Beta Index ETF (Ticker: BUYO). BUYO seeks to provide exposure to selected PE return drivers through a liquid, transparent ETF structure that is more cost-efficient than traditional PE’s standard headline 2&20 fee. This method can be thought of as a “smart beta” approach for PE, providing access to PE-like risk premia within a public market vehicle.

Just as ETFs exist to track broad asset classes like U.S. large-cap and small cap equities, emerging markets, or various segments of fixed income, investors can now access selected PE return drivers through a liquid ETF structure.

Conclusion

As private market funds continue to be adopted quickly in wealth portfolios, we believe it is important to do so with your eyes wide open. As much as you or your clients may believe they don’t need liquidity, they don’t until they do. And if you reach that point where you need liquidity, you better be sure you actually have enough of it.

John Lidington is a Portfolio Manager at Numeric Investors LLC of Man Group and Portfolio Manager of the KraneShares Man Buyout Beta Index ETF (NYSE: BUYO).

For BUYO standard performance, top 10 holdings, risks, and other fund information, please click here.

*Diversification does not ensure a profit or guarantee against a loss. BUYO is non-diversified. The statement regarding diversification refers to sector exposure, not regulatory diversification under the Investment Company Act of 1940.

Citations:

- Data from "Software Stress & AI Risk in Private Credit," Prime Buchholz, as of 2/24/26.

- Data from "Managing the World’s Largest Publicly Traded Hedge Fund: Man Group CEO Robyn Grew," Goldman Sachs.

Index Definitions:

S&P 500 Index: The S&P 500 Index is a market-capitalization-weighted index that tracks the performance of 500 of the largest publicly traded companies in the United States.

Russell 2000 Index: The Russell 2000 Index is a market-capitalization-weighted index that measures the performance of approximately 2,000 small-cap publicly traded companies in the United States.

MSCI Emerging Markets Index: The MSCI Emerging Markets Index is a free float-adjusted, market-capitalization-weighted index that captures large- and mid-cap equities across emerging market countries.

MSCI World ex-US Index: The MSCI World ex USA Index is a free float-adjusted, market-capitalization-weighted index that captures large- and mid-cap equities across developed markets excluding the United States.

ICE BofA US Corporate Index: The ICE BofA US Corporate Index tracks the performance of US dollar-denominated, investment-grade corporate bonds publicly issued in the US domestic market.

ICE BofA US High Yield Index: The ICE BofA US High Yield Index tracks the performance of US dollar-denominated, below-investment-grade corporate bonds that are publicly issued in the US domestic market.