The Alternative Asset Accelerating Into Its Next Phase: California Carbon

After more than two years in the making, California has approved a major overhaul of its cap-and-invest program, the state's primary market-based tool for accelerating investment in low-carbon technologies and one of the fastest-growing commodity markets. This milestone market reform introduces one of the most aggressive supply-tightening schedules in the program's history, accelerating the market’s cap on California carbon allowances (CCAs) by an average annual reduction of 11% out to 2030, compared to the current 4% trajectory.1

For investors, the reform package represents an important inflection point. The accelerated cap decline is expected to shift the market toward a cumulative supply deficit over the next few years. At the same time, California's carbon market remains supported on the downside by its auction reserve price (minimum settlement price at CCA auctions), which is designed to act as an inflation-linked floor that increases annually by 5% plus the Consumer Price Index (CPI).*

Following the Board’s 10–3 approval vote on May 29, CCAs broke out of their tight trading range, moving above the $30 level2 as participants reassessed the forward supply path following the finalized reforms.

A Market Defined by Increasing Supply Scarcity

Cap-and-invest programs operate by setting a declining emissions cap across covered sectors and requiring regulated entities to surrender one allowance per ton of CO₂ emitted. In California, the program covers approximately 80% of statewide emissions, including transportation fuel suppliers, utilities, and large industrial facilities.3 Over time, this declining cap steadily reduces allowance availability, creating increasing supply scarcity and helping to drive long-term price discovery.

Every few years, the market regulator, the California Air Resources Board (CARB), reassesses the market and proposes amendments to better align it with the state’s emission-reduction targets.

This latest reform process under CARB has unfolded over the past two years amid broader economic and political considerations. After initially delaying the rulemaking in July 2024 to accommodate a more comprehensive program redesign and evolving priorities around affordability, federal climate policy uncertainty, wildfire recovery, and concurrent updates to the Low Carbon Fuel Standard (LCFS) market, momentum reignited in September 2025 when Governor Newsom signed legislation extending the program through 2045.

The extension strengthened long-term market certainty and established the foundation for CARB’s updated rulemaking package, which was formally introduced through the Initial Statement of Reasons (ISOR) in January 2026. Following public comment periods and subsequent revisions, the package entered its final stage: the Board meeting vote, which spanned two days, starting on May 28.

Under the approved framework, the emissions cap will decline by 11% annually through 2030 and approximately 7% from 2031 to 2045, materially faster than the existing 4% reduction. In addition, carbon offsets will now be incorporated into the cap, meaning covered entities can meet up to 6% of their compliance obligations through verified emissions reductions from eligible projects such as reforestation, biochar, and carbon capture. Unlike the prior framework, where offsets sat outside the cap, their use now results in a corresponding reduction in the allowance budget, preserving the integrity of the cap trajectory. The reforms also introduce greater flexibility for industrial compliance, including a Manufacturing Decarbonization Initiative (MDI) designed to support emissions reduction investments in California’s manufacturing sector.

The somewhat contentious MDI introduces a new dedicated reserve of 118 million allowances to support industrial competitiveness and decarbonization investment. While the mechanism was a focal point of Board discussion and public comments, several safeguards were introduced at the meeting, including mandatory evaluation and public workshop before credit issuance, and the requirement that any future modifications proceed through a separate rulemaking process.

Given CARB's strong stance on a controlled, closely monitored rollout of MDI credits, the practical volume of MDI supply entering circulation may be limited, particularly in the early years. Even if the full 118 million MDI budget were ultimately deployed, the modeling suggests the bank would still be depleted in 2033, albeit with a much smaller cumulative deficit.4 That said, the combination of the accelerated declining cap and offset-related supply adjustments still results in a broad depletion of the CCA bank over the forecasting period.

Structural Supply Tightening & Long-Term Price Runway

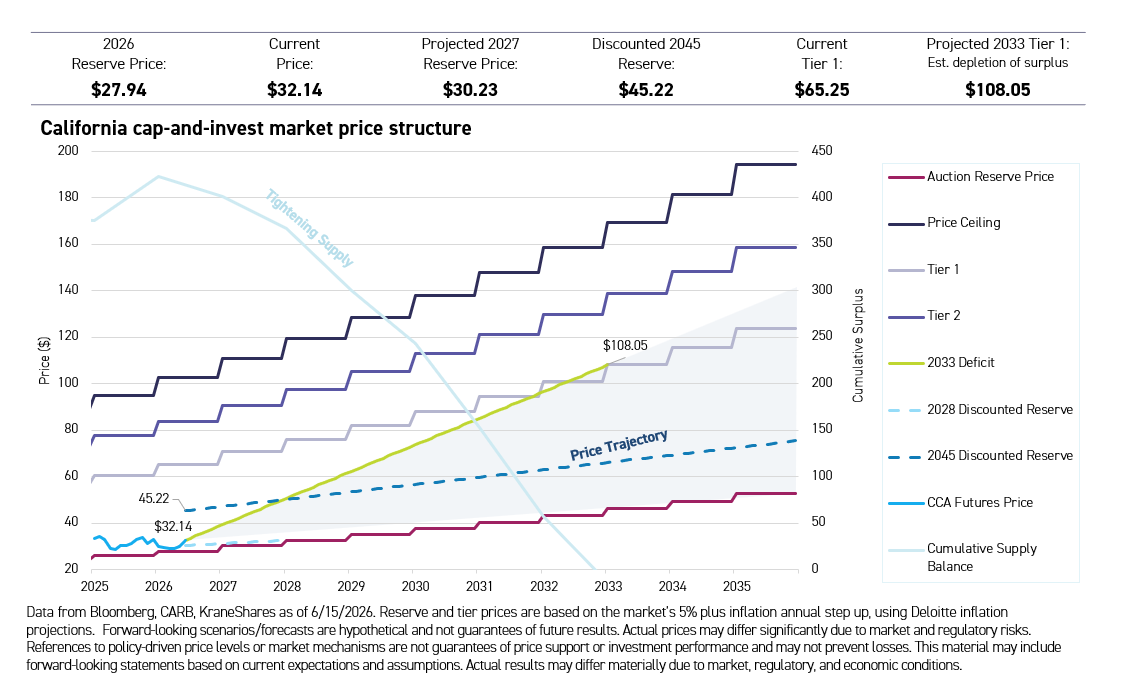

Even with prices rebounding higher, current levels remain substantially below the program’s Tier 1 price containment threshold and the projected long-term reserve price trajectory, leaving meaningful upside potential as supply-demand fundamentals continue to tighten.

For context, the market is structured with both downside support and upper-bound price stability mechanisms:

- On the downside, there is the Auction Reserve Price, which sets a floor price at auctions, i.e., the auction clearing price cannot settle below a predetermined level. In 2026, it is set at $27.94, rising 5% plus CPI annually.

- There are two upper-bound Allowance Price Containment Reserve (APCR) tier levels that serve as a speed bump, releasing additional allowances from a dedicated reserve into the market when prices hit a predefined price trigger to help prevent excessive, uncontrolled price spikes. The Tier 1 trigger price is $65.31 and Tier 2 is $83.92 in 2026, rising by the same 5% plus CPI rate.

- The Price Ceiling serves as a last-resort upper-bound measure, allowing compliance entities to purchase price ceiling 'units' at a predetermined price ($102.52 in 2026, rising 5% plus CPI) if they lack sufficient CCAs to meet their obligation and the APCR tiers have already been exhausted.

Factoring in the reform’s amendments, the cumulative supply balance (light blue line in the chart) is now expected to be fully depleted by 2033. The chart illustrates an implied path from current prices to the level at which the surplus is expected to be exhausted (green line - 2033 Deficit). At that point, prices are expected to potentially hit the Tier 1 level, triggering the release of additional allowances from a dedicated reserve, which the market must absorb before pushing higher.

In present value terms, the current CCA price is approximately 39% below the 2045 discounted reserve price (dotted dark blue line), showing that the market is still at a significant discount to longer-term levels, i.e., the downside reserve floor. Although prices are expected to continue to lift off the reserve floor, this downside mechanism provides further support to the market's long-term price runway.

Investment Implications: Uncorrelated Alternative Asset with Inflation-Linked Downside Support

Combined with the program’s auction reserve mechanism, which rises annually by 5% plus inflation, investors gain exposure to both an embedded inflation-linked support level and a structurally tightening supply profile. Beyond their role as a policy tool, CCAs offer a differentiated real-asset exposure defined by policy-driven supply scarcity, an inflation-linked price floor, and historically low correlation to traditional asset classes.

Unlike conventional commodities, CCAs are not driven by physical production cycles or storage constraints, but by a steadily tightening regulatory cap that shapes long-term price formation. With prices still trading just above the program’s reserve floor ahead of a significant tightening cycle, the market may be approaching an important inflection point as investors reposition for a more constrained supply outlook. For investors seeking portfolio diversification and exposure to a structurally scarce, policy-linked asset class, CCAs may represent a compelling alternative allocation within broader portfolio construction.

Investors can access the market through the KraneShares Carbon Credit ETF suite, with a single market California Carbon Credit ETF (KCCA) and Global Carbon Allowance ETF (KRBN), alongside private offerings for qualified investors.

For KCCA standard performance, top 10 holdings, risks, and other fund information, please click here.

For KRBN standard performance, top 10 holdings, risks, and other fund information, please click here.

Index and Term Definitions:

S&P 500: Standard & Poor's Index is a capitalization-weighted index of 500 stocks.

Bloomberg Barclays US Aggregate Bond Index (”The Agg”): A broad base, market capitalization-weighted bond market index representing intermediate term investment grade bonds traded in the United States. Inception date: January 1, 1986.

S&P GSCI: A composite index of commodities that measures the performance of the commodity market. Inception date: May 7, 2007.

MSCI US REIT Index (daily price return USD): A free float-adjusted market capitalization weighted index that is comprised of equity Real Estate Investment Trusts (REITs). Inception date: June 20, 2005.

MSCI All Country World Index (Gross USD): A market capitalization weighted index designed to provide a broad measure of equity-market performance throughout the world. Inception date: May 31, 1990.

LBMA Gold Price PM: The global benchmark price for global unallocated gold delivered in London, administered by ICE Benchmark Administration® Limited (IBA). Inception date: March 20, 2015.

S&P GSCI Crude Oil Index: Provides a publicly available benchmark for investment performance in the crude oil market. Inception date: May 1, 1991.

S&P Carbon Credit CCA Index: measures the performance of the California Carbon Allowance credit market.

*Consumer Price Index (CPI): is a statistical estimate of the level of prices of goods and services bought for consumption purposes by households. It is calculated as the weighted average price of a market basket of consumer goods and services.

Citations:

- California Air Resources Board, "CARB adopts updates to California’s Cap-and Invest Program to support affordability and align with climate goals," May 29, 2026.

- Data from Bloomberg as of 6/8/2026.

- California Air Resources Board, "CARB adopts updates to California’s Cap-and Invest Program to support affordability and align with climate goals," May 29, 2026.

- Source: Climate Finance Partners as of 6/2/2026.