KVLE US Dividend ETF: A Value-Oriented Approach for a Shifting Market Landscape

By Nathan Eigerman, Director of Quantitative Research & Value Line

From a distance, the stock market may have appeared calm to begin 2026. For weeks, the S&P 500 traded in a narrow range, not straying far from where the year started.

But the markets were far from calm. Closer observers witnessed a violent rotation. Money may not have been flowing into or out of the market as a whole, thus the roughly flat market-wide results, but there was a mad dash from growth-oriented technology (and technology-adjacent) names to less exciting value-oriented ones.

Over the first two months of the year, the Russell 1000 Value index outperformed its Growth counterpart 7.19% to -4.00%.1 In the 47-year history of the Russell indexes, Value has outperformed Growth by that much over two months only during the bursting of the Tech-Telecom bubble in late 2000 and early 2001.

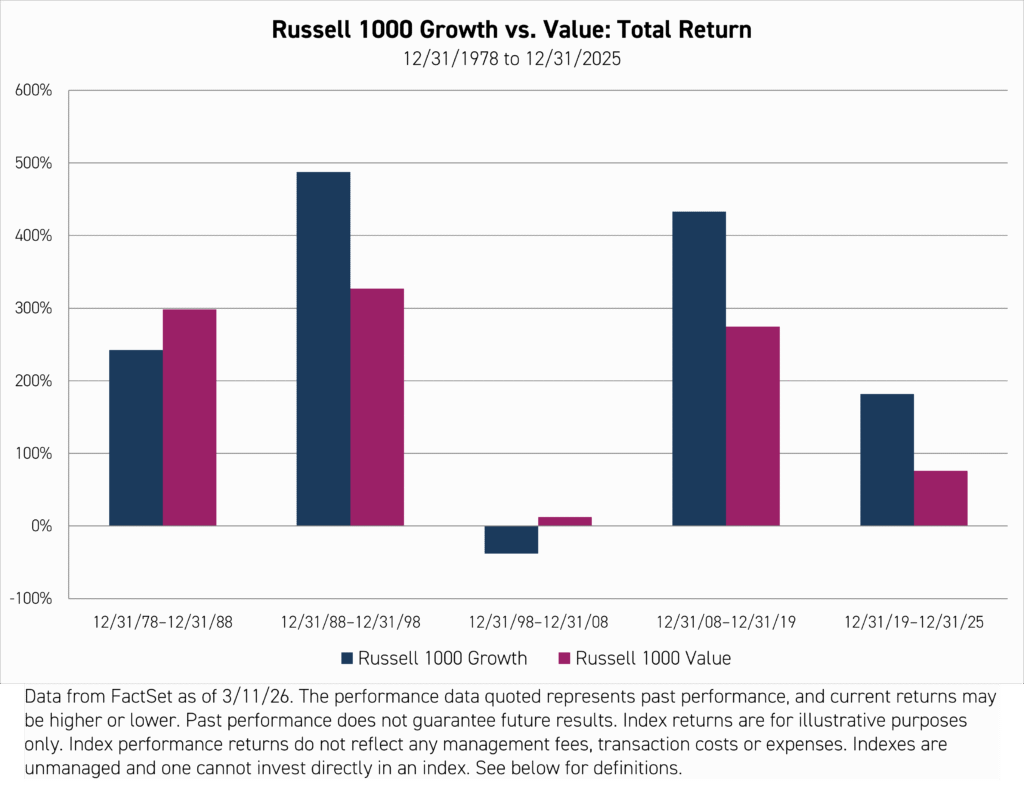

For decades, the Growth and Value indexes did not diverge by much in the long run. Over the 41 years, 12/31/1978 to 12/31/2019, on a total return basis, Value outperformed Growth, modestly, 12.00% to 11.61% annualized.

Then came the COVID pandemic, and Growth steamrolled ahead. From the end of 2019 to the end of 2025, Growth returned 18.90% annualized, against 9.86% for Value. Altogether, over six years, Value gained 76%, which would likely have been satisfactory to most investors had Growth not gained 182% over the same period.

Early 2026 could be a simple correction or the start of a longer-term shift to value. Or maybe something else entirely. In any case, this could be a good juncture for thoughtful investors to reconsider their exposures. For years now, all that has been necessary to beat the market has been to tilt toward growth, particularly the largest growth stocks. That party could be over.

Pundits will sometimes explain market movements as being driven by a “risk-on” or “risk-off” trade. It is not a meaningless description, but it is not very helpful in understanding the choices that confront investors. First, because it implies a binary black-and-white choice, whereas wise risk management would employ shades of grey. And second, because it implies a single monolithic “riskiness” to be modulated by the investor. In fact, the market is not a single risk but the combination of hundreds, if not thousands, of risks.

These past two months have been a powerful demonstration that successful equity investing is more than jamming down on the risk-on accelerator or the risk-off brake at the right moment. The most obvious variety of risk and reward, exposure to the broad market as with an S&P 500 ETF, was largely a non-event through the start of 2026. Slamming the brakes or flooring it had similar results.

But peel a layer off the onion, and you discover that the ho-hum broad market hid a generational shift from growth to value. Which raises the question: which is a better predictor of the long run, the first four decades of the Russell indexes, when growth and value had similar results, or the last six years, in which growth doubled the returns of value? We lean towards the four-decade side, which implies a value-led near future.

Value has been the underdog for so long that many investors may be a little rusty at tilting away from growth. One possible, though aggressive, approach would be to liquidate holdings in core broad-market indexes in favor of less broad value baskets, such as the Russell 1000 Value. But although the Russell indexes are excellent barometers and benchmarks, they may be less efficient for certain value‑focused objectives.

By construction, the Russell 1000 Growth and Value Indexes are designed to each represent approximately 50% of the total market capitalization of the Russell 1000, as every stock in the parent index is allocated to Growth, Value, or a combination of both. That is elegant and useful, but it means that both the growth and value indexes hold some stocks not because they fit with one side, but because they do not fit with the other. Thus, Russell will categorize a company as value if it grows too slowly to be called growth, or as growth if it is too expensive to be value.

Value investors seek to own stocks with attractive characteristics, as measured by commonly used valuation metrics such as the price‑to‑earnings (P/E) ratio or dividend yield, rather than those that fail to meet the criteria for the growth index.

Striking A Balance With KVLE

Our KraneShares Value Line Dynamic Dividend Equity ETF (Ticker: KVLE) has several characteristics designed to align with a value-oriented investment approach.

First, the emphasis is on a higher dividend yield. For us, dividends are attractive less for the payment itself than for the signal they send. A high dividend says that the company has cash to return to shareholders and that management expects that situation to continue. It says management is shareholder-oriented. And it implies that management thinks the company’s stock is undervalued. What is a better example of the ideal of value investing than a company that is prosperous right now and run by management that focuses on shareholders?

Second, KVLE uses the time-tested Value Line Safety and Timeliness rankings to pick stocks. Safety measures the financial stability and volatility of each company. Timeliness is a composite of several factors that together predict 6-12 month relative performance. These rankings are used to select and weight stocks individually. In other words, KVLE follows a bottom-up, diversified stock selection approach, rather than top-down macro or market calls.*

Third, KVLE is benchmark-aware and diversified. Successful investors know that betting a portfolio on One Big Idea is foolish, no matter how attractive. As of the end of February, it is too early to declare a value-driven market. But predicting a less obsessive focus on growth in the future might be justified. Growth has had a historic run these past few years, and if there is one lesson the stock market has taught, it is that eventually the gravitational pull of fundamentals brings even the most widely loved names back down to earth.

For investors utilizing a benchmark-aware approach, this environment underscores the potential benefit of maintaining diversified exposure across both Growth and Value characteristics relative to the Russell 1000, rather than making a concentrated bet on either style.

The goal is to invest across multiple individual ideas designed to provide diversified exposure. Not every idea will pay off, but a diversified approach across multiple return drivers is designed to reduce the impact of any single position on overall portfolio outcomes. So, for example, we might believe that the Magnificent Seven are overpriced, but that does not mean that a risk-managed portfolio should own no shares of those special seven. At around a fourth of the US market, holding the Magnificent Seven without any active position sizing, treating them as a passive, unmanaged exposure, would represent a single large concentrated bet that could dominate the portfolio's relative performance, potentially overshadowing the contribution of all other stock selection decisions. Maintaining significant weights in the more attractive of the Seven, while keeping the group as a whole meaningfully underweight relative to the S&P 500, is a more disciplined, risk-conscious approach to managing this concentration risk.

*Diversification does not ensure a profit or guarantee against a loss.

For KVLE standard performance, top 10 holdings, risks, and other fund information, please click here.

The Value Line® SafetyTM Ranking is based on historical data and applies to the underlying securities of the fund, and not the fund itself. Past performance is no guarantee of future results. SafetyTM does not imply stocks cannot lose value. All investing involves risk including the potential loss of principal.

Citation:

- Data from Bloomberg as of 3/11/26.

Definitions:

- S&P 500 Index: A market capitalization-weighted index tracking the performance of 500 leading publicly traded companies in the United States, broadly representing the large-cap equity market.

- Russell 1000 Growth Index: A subset of the Russell 1000 Index that measures the performance of large-cap U.S. equities with higher price-to-book ratios and higher forecasted and historical growth rates.

- Russell 1000 Value Index: A subset of the Russell 1000 Index that measures the performance of large-cap U.S. equities with lower price-to-book ratios and lower expected and historical growth rates.

- Price‑to‑Earnings (P/E) Ratio: A valuation metric that measures the price investors are willing to pay for each dollar of a company's earnings, calculated by dividing a stock's current price by its earnings per share.

- Dividend Yield: A measure of the annual dividend income generated by a stock relative to its price, expressed as a percentage and calculated by dividing the annual dividend per share by the current stock price.