Can Emerging Markets ETFs Enhance Your Technology Exposure?

Emerging Markets technology is becoming a critical driver of global innovation, offering investors exposure to AI, semiconductors, and digital infrastructure, while trading at lower price-to-earnings multiples than US technology.

US equity valuations remain elevated, and concentration risk is now at a decade-high, driven by a narrow group of mega-cap technology stocks. While we believe US innovation leadership remains strong, some forward-looking portfolios may consider diversification into areas where fundamentals have shown improvement and valuations have been lower relative to US technology, based on selected metrics, such as emerging markets technology.*

We believe the emerging markets (EM) technology sector represents one of the most compelling allocation opportunities right now. Here is why:

A Potentially Weaker US Dollar Supports Emerging Markets Technology Firms.

A softer US dollar has historically been supportive of emerging markets technology and broader EM assets, as local‑currency cash flows translate into more attractive returns for dollar‑based investors. When the dollar is weaker or more range‑bound, financial conditions in many EM economies tend to improve, lowering funding pressures and supporting equity market performance. Policy signals from the current US administration, including its focus on domestic manufacturing and reshoring, imply a tolerance—if not a preference—for a more competitive dollar to support exports, which indirectly enhances the backdrop for emerging markets technology companies linked to global trade and supply chains.

AI Capex Is Powering Asian Emerging Markets Supply Chains.

While artificial intelligence (AI) demand is often discussed through the lens of US mega‑caps, much of the physical build‑out of AI systems actually happens in Asia, led by emerging markets technology companies in semiconductors, memory, and advanced packaging. EM technology firms, including Taiwan Semiconductor Manufacturing (TSMC) and SK Hynix, play important roles in global AI hardware and memory supply chains, and are exposed to ongoing AI capital expenditure ("AI Capex") across data centers, semiconductors, and advanced computing. American companies contract out the manufacturing of their chips to these companies.

Emerging Markets Technology Could Be at an Early Stage of A Potential New Profit Growth Cycle.

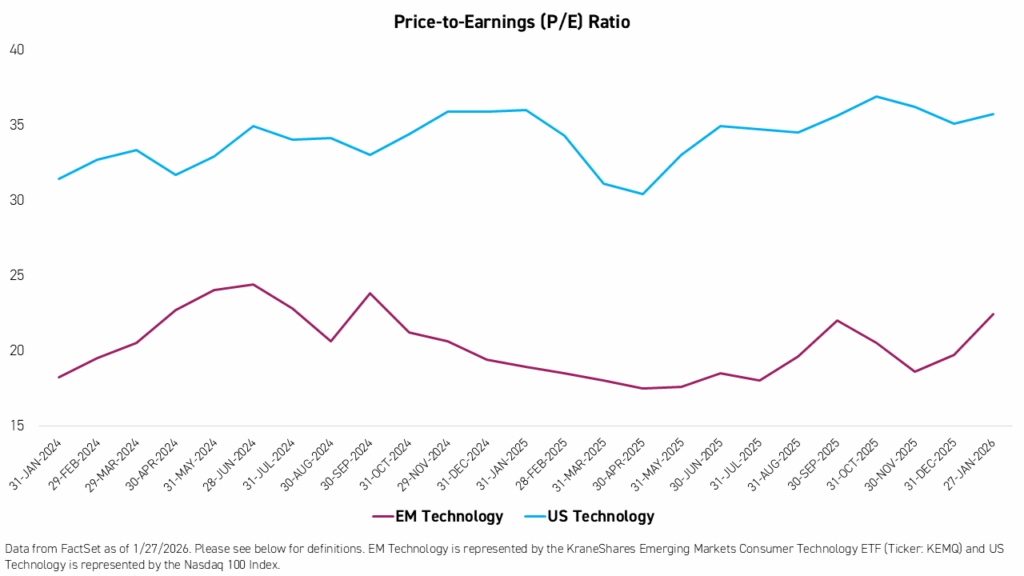

Many EM technology companies recently executed on inventory corrections and cost rationalization that have been viewed positively by analysts.1 Today, we are seeing improving profitability expectations, operating leverage, and balance-sheet metrics, alongside lower price-to-earnings multiples than those f US technology peers.

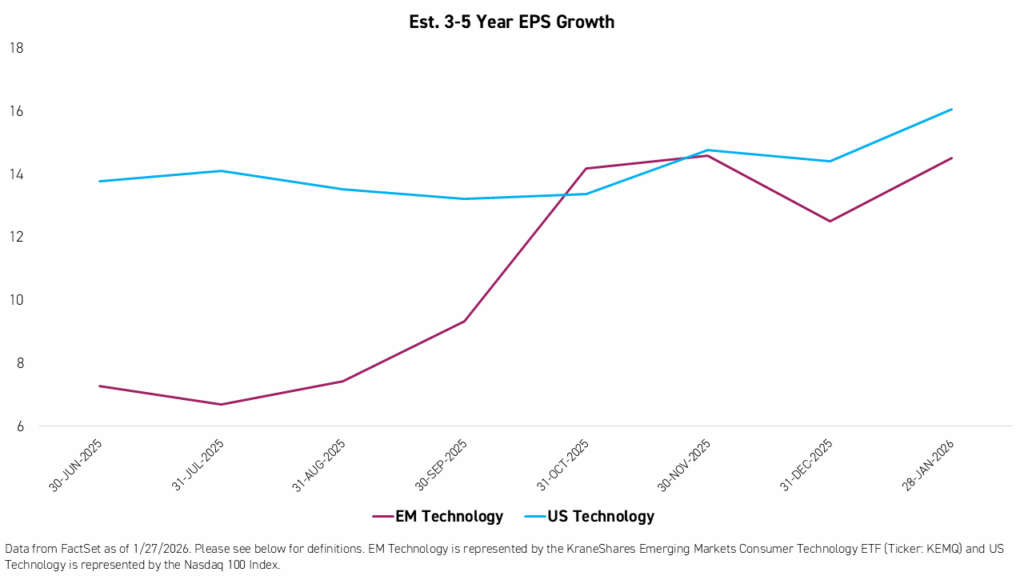

Analysts’ estimates for long-term earnings per share (EPS) growth have also picked up significantly since June, placing them on par with the average estimates for US technology companies.

Due to high concentration in US equities,2 stretched valuations, and AI investment broadening globally,3 we believe EM technology represents a differentiated way to participate in long-term growth themes as part of a broader diversification approach.*

How To Invest in Emerging Markets Technology

The KraneShares Emerging Markets Consumer Technology ETF (Ticker: KEMQ) provides targeted exposure to technology and internet companies across Asia and other emerging markets, positioning investors for this next phase of the global tech cycle. The KraneShares SSE STAR Market 50 Index ETF (Ticker: KSTR) is a potential option for investors to dial-up their exposure to China’s technology sector in addition to broader emerging markets. KSTR provides exposure to the 50 largest companies listed on China’s STAR Market, which is dedicated to companies innovating in information technology, biomedicine, and new energy.

Key holdings in KEMQ include:

SK Hynix (4.3% of Net Assets as of 1/28/2026)

SK Hynix is a South Korean semiconductor manufacturer that specializes in memory chips such as DRAM and NAND flash, as well as related products like SSDs and image sensors. DRAM (dynamic random‑access memory) is the high‑speed, short‑term working memory that computers and servers use to store data they are actively processing, which must be refreshed constantly to retain information. NAND flash is a non‑volatile type of memory that keeps data even when power is turned off and is widely used in solid‑state drives and other storage devices. SK Hynix is one of the world’s largest memory chip makers (commonly ranked second after Samsung) and a key supplier to major global technology companies and data centers, and in recent years it has drawn particular attention for its advanced AI memory, including high‑bandwidth memory (HBM) used in cutting‑edge AI accelerators.

Taiwan Semiconductor Manufacturing Co. (TSMC) (3.76% of Net Assets as of 1/28/2026)

TSMC is a Taiwanese semiconductor company that operates as the world’s leading dedicated contract chip manufacturer, or “pure‑play” foundry. It fabricates advanced logic chips for major global customers, including Apple, Nvidia, AMD, and Qualcomm, powering products from smartphones to cloud data centers and AI supercomputers. TSMC is notable both for its dominant share of the global foundry market and for its cutting-edge process technologies used in the most advanced AI and high-performance computing chips.

Alibaba (3.48% of Net Assets as of 1/28/2026)

Alibaba is a China-based technology platform covering E-Commerce, AI cloud services, logistics, media, and local services. According to publicly reported data, Alibaba’s Qwen large language model (LLM) is one of the most-used models in China and is highly sought after by global corporations.4

For KEMQ standard performance, top 10 holdings, risks, and other fund information, please click here.

Key Holdings in KSTR include:

Cambricon Technologies (10.6% of Net Assets as of 1/28/2026)

A China-based AI chip designer. Cambricon’s processors are increasingly used in local AI servers as China-based companies expand domestic AI computing infrastructure.

Hygon Information (9.9% of Net Assets as of 1/28/2026)

Hygon is a key x86 CPU provider serving China’s data center and AI server markets, Hygon helps power the core computing engines that run cloud and AI workloads. An x86 CPU is a general‑purpose processor based on the widely used x86 instruction set architecture, originally developed for personal computers and now standard in most servers. Because so much existing software, operating systems, and cloud infrastructure is built around x86, these CPUs are the workhorses of modern data centers. Hygon's processors are used in domestic cloud and AI infrastructure as enterprises and hyperscalers expand domestic compute capacity.

Montage Technology (6.4%of Net Assets as of 1/28/2026)

A critical supplier of memory interface and connectivity chips used in AI servers, Montage plays a behind‑the‑scenes but essential role in enabling high‑performance AI workloads. DDR5, the latest generation of double data rate (DDR) memory, allows data to be transferred much faster and more efficiently between processors and memory than prior standards, which is vital for training and running large AI models. By providing DDR5‑compatible memory interface chips and data‑center connectivity solutions, Montage helps ensure that AI servers can move and process the massive volumes of data required for modern artificial intelligence.

For KSTR standard performance, top 10 holdings, risks, and other fund information, please click here.

*Diversification does not ensure a profit or guarantee against a loss.

Citations:

- Medeiros, Gustavo. “A new bull market cycle in Emerging Market equities,” Ashmore. September 2024. Retrieved on 12/31/2025.

- Based on the weight of the top ten constituents in the S&P 500 Index as a percentage of the total index. Data from Bloomberg as of 12/31/2025.

- “Economy.” The 2025 AI Index Report, Stanford HAI. December 31, 2025.

- Jiang, Ben. "Alibaba's Qwen family hits 700 million downloads to lead global open-source AI adoption," South China Morning Post. January 12, 2026.

Definitions:

Price-to-Earnings (P/E) Ratio: A stock valuation metric that shows how much investors are willing to pay for each dollar of a company's earnings, calculated by dividing the current share price by the earnings per share (EPS). It helps assess if a stock is overvalued (high P/E) or undervalued (low P/E) compared to its peers or its own history, often indicating growth expectations (higher P/E) or perceived risk (lower P/E).

Nasdaq 100 Index: The Nasdaq-100 Index tracks 100 of the largest non-financial companies listed on the NASDAQ stock market, including major tech, retail, and healthcare firms, and was launched on January 31, 1985, as a benchmark for innovation-driven growth, not including financial firms.

Earnings per Share (EPS): A company's total profit over a 12-month period divided by the number of shares outstanding.

Est. 3-5 Year EPS Growth: Annualized growth expected for a company's earnings per share over at least a three year period. For the purposes of this communication, publicly available estimates as far into the future as five but no less than three years are used for the constituents of an index or holdings of a fund to generate a harmonized average.